Founders are often puzzled by how VCs derive valuations for competitive Series A rounds. A competitive Series A round is an equity round where a company generally raises greater than $5 million led by a top-quartile venture capital firm.

During these Series A rounds, it is not uncommon for founders to receive multiple term sheets from lead investors at different valuations, and to feel uncertain about how to come to the correct valuation for the company.

The cause for this confusion is that VC valuation processes are often a black box, where there is no industry standard methodology for calculating valuation of seed to Series A startups. Some investors suggest that their valuations are a function of users, revenues, market potential or other forms of company traction, while others cite comparable deals as the primary justification for valuation.

There are VC firms that attempt to use the “VC Method,” but the VC Method breaks down when dealing with very early stage startups that often have little financial data and few comparable companies.

Finally, some investors admit that they are pulling the number from the sky, or are simply willing to pay more than other investors to win the deal. Generally, the valuation range results in the group of Series A investors taking 15-25 percent of the company.

Although there is no industry standard methodology for calculating Series A valuations, the reality is that arbitrarily accepting (or setting) a Series A valuation can do more damage than good for a company’s future funding or exit opportunities. If the valuation you choose is much lower than the intrinsic value of the startup, it can cause you to give up too great a share of your company.

Alternatively, if the valuation is too high, you may face a down round at your Series B. Savvy founders are aware of the risk of an incorrectly priced Series A round, and are often in search of a reasonable framework for estimating the right price for their Series A. This article attempts to provide that framework.

My partner and I at 645 Ventures work closely with our seed-stage founders to help them raise competitive Series A rounds. As part of this process, we help our founders think through establishing the right valuation range for their company, which we sometimes refer to as the market-efficient price of the round. We have not developed a magic formula that computes valuations given specific inputs.

Arbitrarily accepting (or setting) a Series A valuation can do more damage than good for a company’s future funding or exit opportunities.

Every early stage startup is different, and there are so many distinct attributes of a company’s value that such a formula would have too many parameters to be meaningful. Instead of using a silver bullet formula, we focus on determining the valuation that is a reflection of the milestones reached by the startup team, while at the same time reflects reasonable foreseeable future performance.

It is important to note that the market-efficient price leaves room to raise future rounds at realistic higher valuation ranges, is low enough to make a future acquisition possible for the right acquirer and is rewarding for the startup team and its employees. To get to the right price there often is a trade-off between how much capital the company needs and how much equity the team is willing to give up.

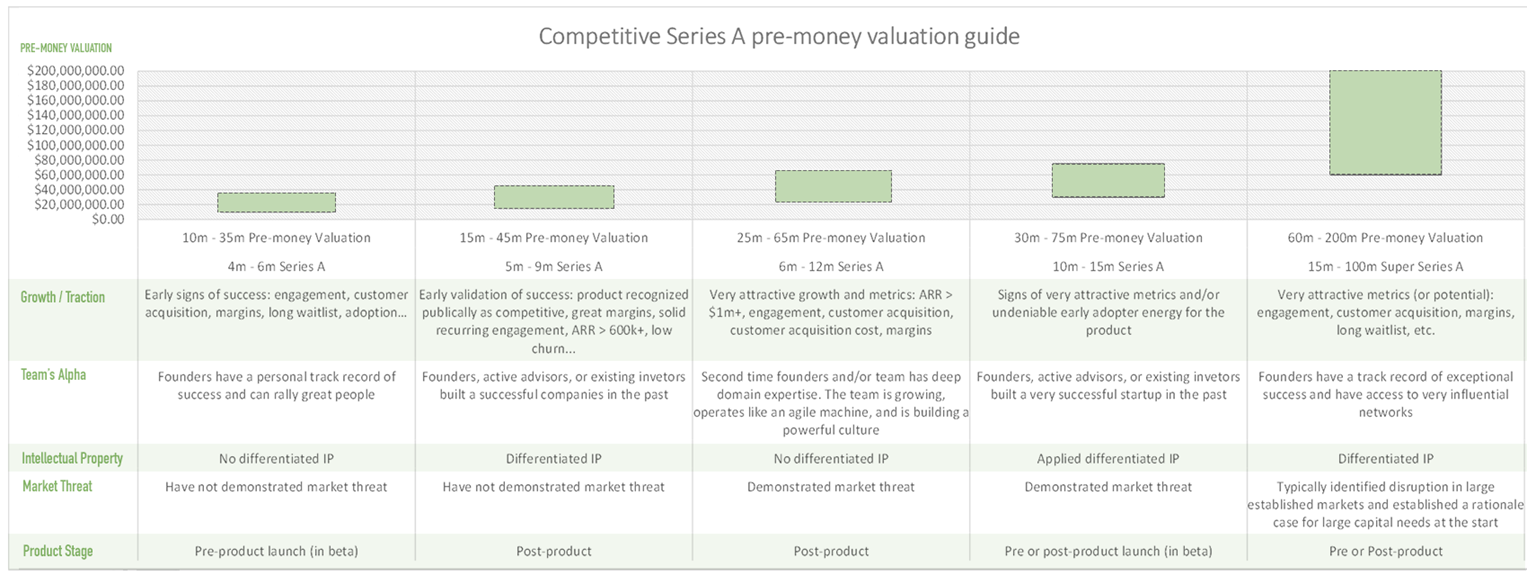

We encourage founders to initially think of the value of their startups based on five categories: market threat or expansion, the team’s alpha, intellectual property, product stage and growth rate (the most commonly applied rationale).

Below is a graph that shows a general set of Series A valuation ranges, demonstrating how these factors can impact pre-money valuations. Below the graph is greater detail on market, IP and growth impact on valuation.

Note: Super Series A rounds are relatively new, having emerged around 2012. They are indicative of a more exuberant market, where large seed round sizes have expanded to what was previously the average Series A round size, and the largest Series A round sizes have expanded to what was previously the average size of growth rounds (i.e., Oscar, Compass, Jet, Maple, GitHub, etc.). Super Series A rounds are generally started by above-average founders with significant social, entrepreneurial and sometimes political influence.

Market Threat Or Expansion Opportunity

When a new company has built a product or service that undeniably threatens large incumbents, we find that there is often a correlation between the company’s Series A valuation and competitors’ balance sheets, market capitalizations and trading multiples.

We define an undeniable threat as a team’s demonstrated ability to build products/services that are rapidly stealing market share from large incumbents because the new product is significantly better, faster or cheaper.

If the new company’s growth continues, then the incumbent can be in danger of losing substantial market share. This can be the case in either consumer or B2B markets. When threatened by a new company, incumbents can respond by acquiring their competitor and expanding their own market position.

To get to the right price there often is a trade-off between how much capital the company needs and how much equity the team is willing to give up.

For example, think back to Facebook (incumbent) versus Instagram or Snapchat. Facebook is the largest social network on the planet, as well as the largest photo-sharing site on the web. Both Instagram and Snapchat threatened Facebook’s core value proposition, and both did it on mobile, the most important platform that Facebook had not yet dominated. These threats contributed to Facebook’s acquisition of Instagram and to its attempted acquisition of Snapchat.

Because of Facebook’s large balance sheet, the market threat (and corresponding expansion opportunity) posed by Instagram and Snapchat positively impacted their valuation potential. If you assumed Facebook would spend up to 1 percent of its future market cap (now valued at $274 billion) to protect its market position, then we could assume Facebook would be willing to pay multiple billion of dollars to eliminate its most significant threats.

In valuing these companies at the Series A, both prospective investors and founders would have taken into account future potential acquisition value.

Another consideration is to assume that both current customers/users and future customers/users have value that can be monetized. In cases of non-revenue-generating companies, valuation can be calculated by the revenue per user of the incumbent ratio discounted by 20 percent or more due to required multiple expansion at exit and uncertainty of future startup growth.

For B2B or revenue-generating companies, applying the trading multiples (i.e., TEV/Rev) of the incumbent to foreseeable growth targets, then applying similar discount rates, is a good method for calculating valuation.

If you are a founder, proving your company is a market threat (or an expansion opportunity) for an incumbent and receiving an acquisition offer usually makes your company far more desirable in the eyes of an investor.

At the same time, if you’re lucky enough to be in this scenario, be careful not to overvalue your company, especially when compared against an acquisition offer. An acquisition offer is certainly a great benchmark; however, founders should not over-leverage that demand to drive up the Series A valuation. Make sure your price is consistent with purchasing power of acquirers, and leave room for subsequent up rounds.

Intellectual Property

Differentiated intellectual property with mass commercial application and broad market demand is difficult to come by in the world of Internet and software startups. However, when a team owns such IP, has a well-defined product roadmap and has significant excitement from early adopters, that company may be in a position to influence the creation of a new market or product category.

The risk of product adoption is uncertain for nascent markets; however, the opportunity for differentiated IP to create a new market category can outweigh adoption risk. Both startup founders and investors have to swing for the fences in this case. This scenario can lead to competitive valuations when the founding team has the right skills, timing and investment runway.

Recently, this type of IP has appeared in the form of hardware (i.e., Internet of Things/connected devices), open-source technology with defensible communities and advanced software algorithms, including computer vision, machine learning, natural language process and security. What makes businesses with these categories of IP so valuable is that they can be difficult to replicate.

With regard to valuation, differentiated IP can give early stage companies a valuation premium above what growth and/or market threat can provide. A team’s ability to build real IP and high-complexity software with mass commercial appeal creates confidence in the defensibility and value of a startup.

Recent examples of proprietary IP driving up valuation are Nest (market expansion), Oculus Rift (new market creation) and Elastic Search (market enabling and open source).

Growth

Unfortunately, the majority of companies cannot be valued based on undeniable evidence that the company is market-threatening, or that the company has IP that can create a new product category. Therefore, most startups rely on the future promise of building something transformative combined with historical evidence of growth.

Evidence of growth usually takes the form of demonstrated engagement, such as user growth and retention, talent acquisition and execution ability. How growth metrics impact valuations can also vary based on industry and customer segmentation: consumer versus enterprise, online marketplaces versus direct sales, etc.

For each industry and customer segmentation, great founders establish a set of, and track, Key Performance Indicators (KPIs) that are indicative of demand, adoption, profitability and scale.

It’s important to note that foreseeable and projected growth are key drivers of generating term sheet interest, and not purely a basis for valuation. The goal is to get investors so excited about the promise of your company that you get term sheets from investors who have been involved with similar success stories.

Receiving Series A term sheets from these types of investors helps founders set competitive valuations. Once this competitive position is established, then growth numbers can help justify the valuation that is right for the startup. Below are a couple of examples.

Revenue-Generating Companies

When you start discussing revenue with investors, be aware that this discussion will likely prompt additional questions. The questions that inevitably follow a revenue discussion pertain to customer lifetime value (CLV), customer acquisition costs (CAC), margins and churn.

Great investors will determine whether revenue growth is sustainable, as well as whether unit economics are sound, thus driving underlying profitability. If founders prove their company has a sound economic model and growth in a large or expanding market, then valuation can be based on a multiple of projected revenue over foreseeable runway. For most revenue-generating early stage software companies, Enterprise Value to Revenue (EV/Revenue) can be an appropriate multiple.

In low-margin businesses, which include transaction-based startups, marketplaces, affiliate networks, etc., Enterprise Value to Net Revenue (EV/ Net Revenue) is a better indicator. Most importantly for competitive Series A rounds, there are often revenue thresholds that must be seriously considered: $1 million+ ARR for enterprise deals, $10 million+ for marketplaces and $1 million+ of pre-orders for direct consumer products.

Apps And Product Companies

For pre-revenue companies with user-growth figures, a total number of downloads greater than 1 million can be a good starting point for a VC conversation. However, what’s more important than absolute user growth are engagement numbers: viral coefficients, transactions processed per day, Daily/Monthly Active Users (D/MAUs), data generated per day or month, cohort performance, average time on the platform, etc.

These numbers help founders tell a ready scale story. These companies are difficult to value, but using the Competitive Series A Pre-money Valuation Guide can help direct the valuation.

While there isn’t one way to value a company, these are some of the techniques we share with our founders when working with them to price competitive Series A rounds. The exercise of valuing your company will leave you more prepared to understand the terms you receive from lead investors, and armed with information with which to negotiate terms.

The beauty of startup finance is that it is an art and a science, so the valuation methods you use should give you a valuation range. Closing the deal ultimately requires a delicate balance of new investors’ ownership interests and existing shareholders perception of value and growth expectations.