Varied explanations for the growing herd of unicorns — and predictions of their imminent demise — abound. But all can agree: Those who invest in unicorns are chasing returns they can’t get elsewhere. And while venture capital is widely perceived to be fueling the unicorns’ growth, a closer look reveals that not all venture capital is really venture capital.

Data on VC fundraising shows a long-term decline in capital to VC funds, a trend I covered here. If less money goes in, less is available to be deployed.

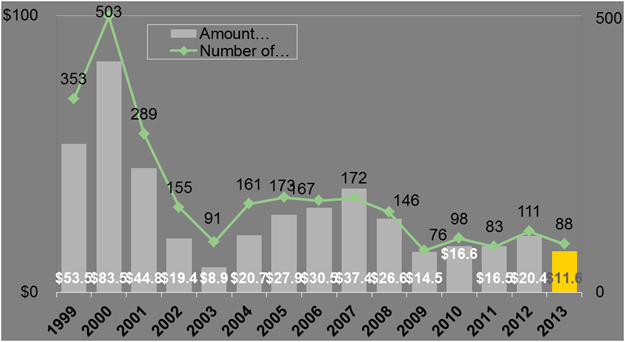

Declining fundraising in the U.S. since 2007. 2009 marks the fewest funds raised in 16 years. 2009 was the low point in terms of dollars raised since 2003.

In 2014, Dow Jones reported that the amount of venture capital invested in the United States soared to $52 billion, from $35 billion in 2013, an increase of almost 50 percent. How could VC investment increase when VC fundraising declined?

The answer is semantics. The cash that’s now being called “venture capital” isn’t truly venture capital. Instead, the mystery money is coming from asset classes such as mutual funds, hedge funds, private equity funds and corporate venture capital that have started actively investing in venture-backed technology companies. That money explains the rapid rise in investments into venture-backed companies during the past two years.

Because we can’t see into the unicorns’ capitalization tables, these asset classes have been lumped together as “venture capital.” But these mutual, hedge and private equity funds have vastly more capital at their disposal than traditional venture capitalists. Preqin data shows the hedge fund asset class alone has approximately $3.5 trillion of investment capital.

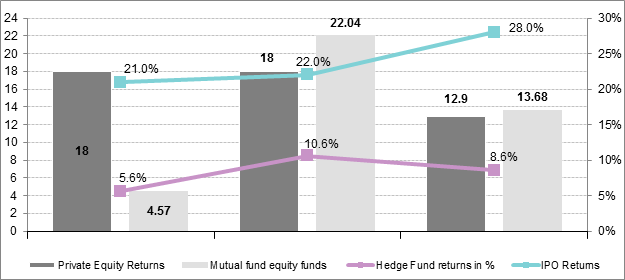

Why would these asset classes, which have traditionally shunned private technology companies, suddenly embrace them? The answer may lie in the IPO market resurgence. During 2013 and 2014, IPOs produced returns that outperformed the broader markets and that, in many cases, greatly exceeded other asset classes.

Asset Class Returns

Sources: Private equity: Dealogic; IPO returns: Dealogic; Hedge funds: Eureka North American Hedge Fund Index returns; Mutual funds return: Strategic Insight/SimFund MF

In today’s zero interest rate environment, these investors are effectively “buying down” into the venture asset class, hoping to capture higher returns. And who could blame them? The past two years have seen numerous opportunities to invest in companies in their final round of private financing with a quick path to an IPO. To sweeten the pot, many of these investors also have investment vehicles that purchase IPO stock.

The investment thesis goes like this: Non-venture capital investors buy into the last private round of funding. At the IPO, the valuation is expected to increase significantly over the last private round. In addition, these investors expect a healthy first day IPO stock price pop, which will bolster returns even more.

In the past two years, driven by the mobility trend, numerous companies have achieved incredible scale, raising mega-rounds of financing from these non-venture capital investors. The result has been substantial growth in the unicorn population.

The venture capital business is a marathon, not a sprint.

Given the rush of additional asset classes investing in venture capital-backed technology companies, unicorns and unicorn-wannabes are heeding market wisdom and raising capital now, while it’s available. This has led to a flurry of mega-round financings that ensure companies have ample capital available should the financing environment change. The result has been a frothy environment, especially at the later stages.

Eventually, something will cause these non-venture capital investors to stop investing in tech companies and refocus on their core areas. When that happens, several things will occur. First, companies in the VC pipeline will need to focus on execution, as additional rounds of capital won’t be as readily available.

Second, these companies will likely stay private longer because many will have the cash to do so and will need to grow into the valuations they have achieved, especially at the later stage of the market.

Finally, the chances of seeing a first-day IPO stock price pop will diminish as companies at the later stages price themselves close to perfection in the private markets.

These large investments in technology companies may not be as risky as people think. The investors with the most valuation exposure aren’t VCs, but rather hedge, private equity and mutual funds. Compared with VCs, they are highly diversified investors. If a slowdown were to result in some down rounds in the unicorn population, the overall market could likely weather it.

The venture capital business is a marathon, not a sprint. So, if market dynamics force a pause, that’s okay, especially for well-capitalized companies.

And given the global nature of the trend toward mobility and platform-shifting to smartphones and tablets, we are early in a long-term opportunity. The effect of this trend will be transformational, and venture capital-backed companies will play a big role.

While comparisons to the late-90s bubble are inevitable, the froth is different this time. It’s in later-stage companies and being driven by different forces and investors. My definition of a bubble is when a majority of the asset class is overvalued.

The unicorns are driving today’s bubble conversation and, despite their outsized press, only amount to fewer than 150 companies out of nearly 5,000 venture capital-backed companies. Because of that, I’m not ready to call a VC bubble.