A startup whose first product is a mobile money management application called Even, designed to offer low-income workers interest-free credit to help them make ends meet in between paychecks, has raised $1.5 million in a seed round led by Keith Rabois of Khosla Ventures, with participation from other investors. The service is meant to offer hourly, and generally part-time workers an alternative to riskier payday loans and other lending products where debt compounds, making it even more difficult to recover from life’s curveballs.

Other investors in the round included Homebrew, Kevin Systrom, Mike Krieger, Michelle Wilson (former general counsel of Amazon), David Tisch, Adam Rothenberg, Sam Lessin, Slow Ventures, Red Swan, Andrew Fine, Zach Brock, Joe Ziemer, Andrew Kortina (Venmo).

One of the worst injustices about the income inequality situation in the U.S. is just how expensive it is to be poor. Setbacks that others would consider inconveniences can actually ruin your life, explains author Linda Tirado, in her book “Hand to Mouth: Living in Bootstrap America,” which details what it’s like to live in poverty as low-wage worker. In one story, she explains how a minor annoyance to most of us – getting her car towed – ultimately cost her both of her jobs, and soon after, her apartment.

Unfortunately, much of the consumer-facing technology emerging from Silicon Valley is focused on serving the needs of the better-off, where just about anything can now be ordered on demand from groceries to black cars to even manservants or just cookies. There’s definitely growth potential in portions of this market, as Uber-watchers could tell you, but the companies that emerge don’t always meet the needs of the many.

According to the U.S. Census Bureau, 45.3 million live in poverty in the U.S. in 2013. Nearly half of Americans in major cities live in a state of financial insecurity, and many turn to alternative – and often predatory – lending services when times are tough.

Even also reports that there are now 51 million in America who spend an average of $1,000 per year on things you “pretty much get for free at a bank.”

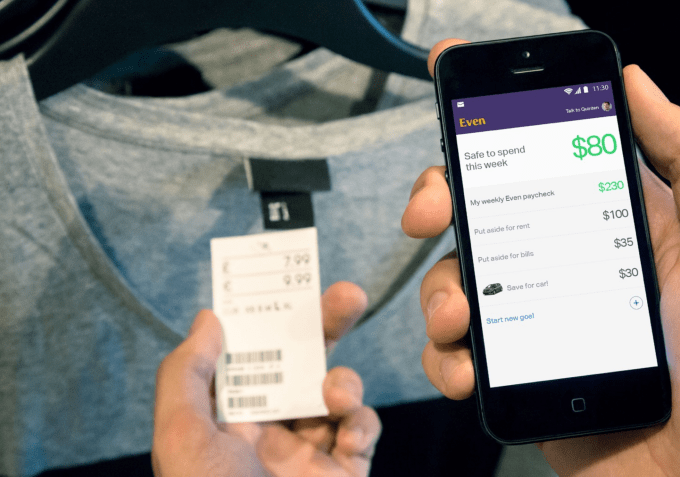

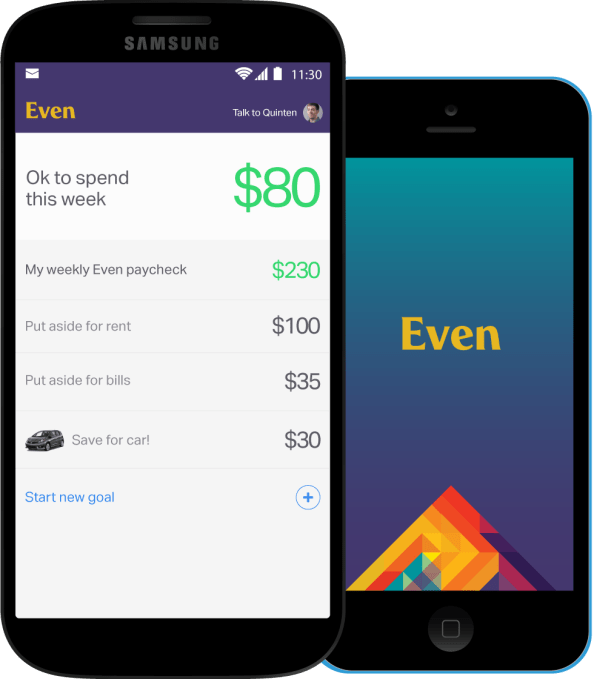

The company’s big idea? To offer consumers interest-free credit that helps them during bad weeks. The way the product works is not at all like payday lenders, though they’re targeting the same market. Customers using Even will authorize the company to manage their money for them. During good weeks, it sets a little money aside on your behalf, then, during the not-so-good weeks, users can tap into credit to pay their bills, or deal with whatever other expenses come up.

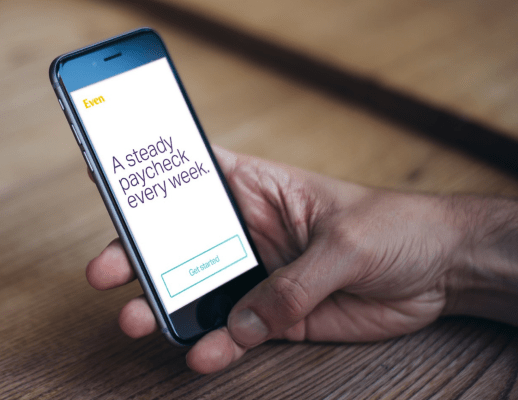

The program, available to consumers via a mobile app, is still in pilot testing, meaning a lot of the finer details are still being worked out. However, the end result is that customers receive a steady paycheck of the same amount from week to week, even as they work more hours some weeks, and fewer on other weeks.

The service works with a customer’s own bank account, and offers a number of features including automatic budgeting, help for emergency expenses, and even a “pause” button for when you need to turn off the $5/week charge while you recover from a hardship, like a job loss.

Instead of making it more difficult to pay back the debt, the idea is to be lenient – taking as little as a $1 per week, if need be, while maintaining the customer relationship during the bad times.

“It’s kind of like insurance,” says co-founder Jon Schlossberg. “You pay a flat monthly fee for coverage.”

It’s still expensive to be poor: Even would cost $260/year, but it’s less expensive than getting into trouble with payday lenders. It could also mean that bills and rent get paid on time, which could potentially break the cycle where a single bad break, or a week with reduced hours, can snowball into homelessness.

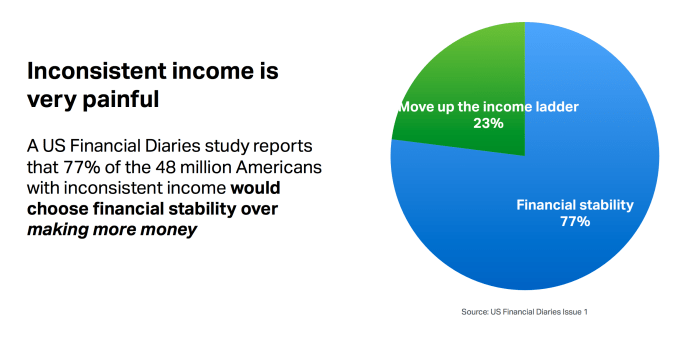

Citing a U.S. government research study, Schlossberg says he was blown away by learning that 77% of Americans reported they would rather have more consistent income than make more money. A self-admitted “privileged white male,” he realizes that having everything come easy is not the case for most, he says.

“Just wanting money to be there every week is one hardship I’ve never experienced…that’s something that’s kind of hidden from Silicon Valley” Jon Schlossberg

“Just wanting money to be there every week is one hardship I’ve never experienced…that’s something that’s kind of hidden from Silicon Valley,” says Schlossberg. “The problem is income volatility.” What’s increasingly happening, he explains, is that as the workforce shifts towards more flexible labor, part-time workers end up with inconsistent hours. This issue was recently detailed in a New York Times profile of Starbucks barista Jannette Navarro, whose ever-fluctuating hours at the popular coffee chain were due to Starbucks’ reliance on employee scheduling software, designed to boost profits, not make workers’ lives easier.

In addition to its $5 per week consumer-facing service, Even is also selling to enterprise, and has at least one deal in discussions with a large business that you “visit weekly.” (Starbucks?,” I guessed. “No comment.”) With corporate customers, Even could be offered a company benefit – potentially even boosting the bottom line due to the high costs associated with part-time turnover, associated with the shift scheduling issues. (U.S. businesses see 69% turnover for part-timers vs. 23% for full-time workers, excluding seasonal labor, Even reports.).

The company is based in Oakland in order to strategically place itself closer to potential customers. In addition to product designer Schlossberg, previously of Bonobos, its founding team includes designer and engineer, Ryan Gomba previously of Instagram, who worked on the iOS app; Cem Kent, previously of Taykey; and Quinten Farmer, who earlier tried to tackle the student loan problem via The Open Loans Project.

Schlossberg acknowledges that they don’t know if the business model of charging $5/week will work, because there are a still a lot of unknowns the pilot is attempting to figure out like the average credit utilization or how much they’ll lose on defaulted credit. But he does say that the big businesses they’ve talked to so far are “extremely receptive to this product.”

“If we’re right, it’s a win for their company, it’s a win for the employees because their lives are meaningfully improved, and it’s a win for us because it gives us distribution into a market that’s vastly underserved,” says Schlossberg.

Even expects to launch publicly this year, though users can request an invite now.