Strict new price caps will come into force in the U.K.’s payday loans market in January, sector regulator the Financial Conduct Authority (FCA) has confirmed, affecting any U.K. businesses that offer this type of short-term consumer credit.

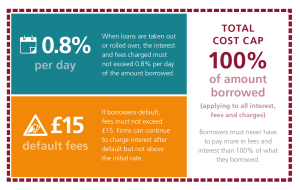

The FCA said today that from January 2, 2015 it will be imposing an initial cost cap of 0.8 per cent per day for all high-cost short-term credit loans, which means interest and fees must not exceed 0.8 per cent per day of the amount borrowed.

It will also be applying a total cost cap of 100 per cent on a loan, meaning a borrower must never pay back more than 100 per cent of the amount they borrowed in order to protect them from escalating debts. Fixed default fees are also capped at £15 for borrowers who do not make loan repayments on time. And interest on unpaid balances and default charges must not exceed the initial rate.

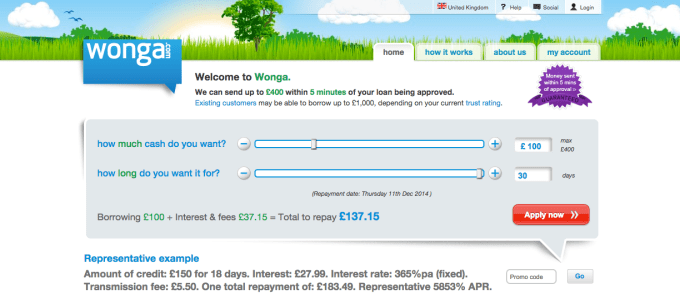

The result of the regulatory caps will be a far smaller payday loans market, and one which can’t generate huge profits at the expense of the most vulnerable borrowers. Last year one payday loans company, Wonga, listed its representative annual interest rate at 5,853 per cent.

In the first five months since the FCA has been regulating the sector it said the number of loans and the amount borrowed has dropped by 35 per cent. Going forward, it is estimating the new price caps will mean seven per cent of current borrowers may no longer have access to payday loans — some 70,000 people.

In the first five months since the FCA has been regulating the sector it said the number of loans and the amount borrowed has dropped by 35 per cent. Going forward, it is estimating the new price caps will mean seven per cent of current borrowers may no longer have access to payday loans — some 70,000 people.

“These are people who are likely to have been in a worse situation if they had been granted a loan. So the price cap protects them,” it notes.

Caps on the payday loans market have been expected since 2013, when the duty to cap the cost of credit was formally established through the Financial Services (Banking Reform) Act 2013. The FCA spent this summer consulting on its proposed caps and has today confirmed the levels it was consulting on.

“I am confident that the new rules strike the right balance for firms and consumers. If the price cap was any lower, then we risk not having a viable market, any higher and there would not be adequate protection for borrowers,” said Martin Wheatley, the FCA’s chief executive officer, in a statement.

“For people who struggle to repay, we believe the new rules will put an end to spiralling payday debts. For most of the borrowers who do pay back their loans on time, the cap on fees and charges represents substantial protections.”

The FCA notes that from January 2, no borrower will ever pay back more than twice what they borrowed, while someone taking out a loan for 30 days and repaying on time will not pay more than £24 in fees and charges per £100 borrowed.

Wonga still looks to be charging higher rates of interest and fees than the impending price caps will allow. A loan fee calculator on its website states that a £100 loan taken out for 30 days will incur interest and fees of £37.15. But from January 2 the same loan will have its interest and fees capped at £24.

Last month Wonga was forced by the FCA to write off the debts of some 330,000 customers, and waive the fees and charges of a further 45,000 — taking a write down of around £220 million — after admitting its affordability checks had been inadequate.

It has put in place interim measures to test affordability, and is in the process of rolling out a new permanent lending decision platform that reflects the new affordability criteria. But the company — which for years touted the speed and efficiency of its technology platform in making lending decisions — will clearly see its business shrink further when the new price caps come into place.