Editor’s note: Andreas Penna is managing director and founder of Penna & Company, an M&A and investment advisory firm. He is also an angel investor.

2014 has seen an unprecedented number of M&A transactions globally, especially within the tech sector. Global tech M&A was up 55 percent over last year, soaring to its highest level since 2000. Technology-related transactions this year alone have generated over $100 billion.

Now, we’ve all heard of the large-scale, headline-grabbing mega acquisitions of WhatsApp, Nest, Beats, Oculus VR, and Waze. They are fodder for startup founders, and beacons of hope for bleary-eyed entrepreneurs striving for fortunes. But while these large-scale M&A transactions have been basking in the media glow, a number of smaller deals have been forged in the tech hot spot largely in Silicon Valley. Recently, the tech world is pumping with M&A activity, from small aqui-hires to large super deals.

The M&A spell is being driven by the move to mobile. During the past 12 months, mobile Internet M&A has seen $47 billion in total deal value. Mobile focused M&A alone is up 5X from the previous year. When excluding the WhatsApp deal, 50 percent of the largest remaining M&A segments in mobile are games, messaging, music and food and drink, according to Digi Capital.

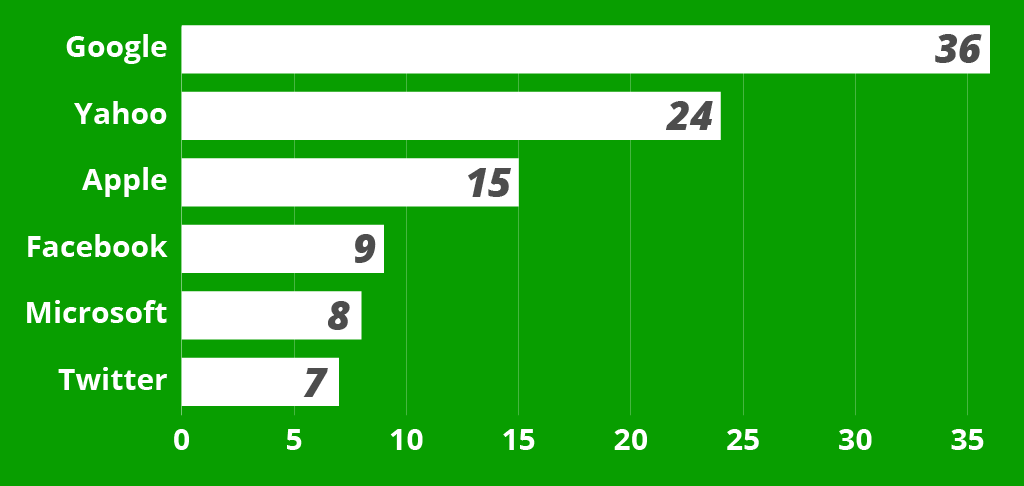

Mary Meeker’s latest Internet trends evaluated the big buyers globally and show major competition for top acquirers. From 2012 to May 2014, M&A transactions from Facebook were $24 billion, with Google and Alibaba in hot pursuit at $6 billion and $5 billion, respectively. The following chart breaks down the number of deals that have transacted among major U.S. tech players in the last 12 months:

So what’s driving the recent M&A frenzy by large tech buyers? There are several key catalysts: high stock prices, large cash piles, spend versus investor dividends and talent acquisition. These potent factors have helped brew a highly competitive environment that has thrust M&A into overdrive. Big tech companies are in an all-out sprint to snap up relevant companies, especially when it comes to IP and user base acquisitions.

Despite this M&A frenzy, many companies seem to be painfully unaware of the critical variables in the valuation equation. When approached by a potential acquirer, most CEOs are in the dark. While they understand the ins and outs of venture capital raises, more often than not they have little understanding of multiples and valuation approaches in the M&A world.

For those of you out there who want a quick breakdown of the basics, here is my abridged version of how to calculate an acquisition valuation: Acqui-hire value + return of investor capital + premium = total acquisition valuation.

Acqui-hire value: At current Silicon Valley prices, valuation per engineering employee is $1 million to $2 million USD over a four-to-five-year period. The exact number of engineers absorbed depends on the individual interviews.

In this scenario, non-engineering assets are typically not absorbed, except where there are local marketing needs, exceptional talent and key executive management members. If this becomes an M&A transaction around acquiring a subsidiary, then the entire HR assets are likely to stay intact. In either scenario, companies will provide a term sheet that takes into account a total compensation package per employee over four to five years (of which stocks and options will vest over this time period).

Return of investor capital: This is typically paid out at around at least 100 percent, and investors get the capital back first.

Premium: There are a few premiums that must be considered in order to calculate this figure:

- IP / patents, value

- Make versus buy value

- Positive cash flow businesses value

- Competitive disadvantage value (removing a target from potential competitor acquisition)

6 Tips for CEOs looking to shop their companies

When opportunity comes knocking on your door, you want to be ready. It will officially be game day, and you better hope that you’ve warmed up, stretched, laced up your shoes and strapped on your helmet. Want to be the pinnacle of preparedness? Follow these rules.

- Do your due diligence. Figure out exactly why and how a company is valuing you. Are they looking to capture your value before a competitor does? Do they want your IP? Or are they looking to welcome your highly talented team? Unearthing these answers will provide you critical insight into how you can position yourself during negotiations.

- Get a solid BATNA (Best Alternative to a Negotiated Agreement). You should strive mercilessly to establish a BATNA. How do you accomplish this? By shopping your company on the market! Push as hard as you can to get offers and counter offers. Doing so will help you seamlessly employ the classic market bidding principle: the more bidders there are, the higher the price of an asset.

- Find a senior internal executive sponsor. When establishing your BATNA, it is essential that you connect with the right internal executive sponsor (or close to C-level individual). Decision makers, especially for M&A, are concentrated at the top ranks of most acquiring companies. If you don’t have access to these folks, find an adviser who does.

- Know the basics of capital and asset structuring. Make sure you understand the different capital and asset structures for a deal, e.g. upfront versus cash outlays deals, stock deals and equity vesting schedules to name a few.

- Familiarize yourself with various acquisition approaches. Understand the assortment of different acquisition approaches. These will vary based on the particular reason why a company is interested in making an acquisition. For example, if a company is seeking an acquihire, it’s often easiest to release employees from the corporate entity and close it down separately. This strategy reduces liabilities and risks while lowering the legal bills on both sides. If it’s IP they’re after, there are highly nuanced ways in which to spin this out while maintaining the structural integrity of the target company (for those interested in continuing operations). The bottom line is this: Acquiring companies can have many motivations; figure out what is driving the deal and use that to your advantage.

- Retain a top-brass independent startup lawyer. You will inevitably need a lawyer. When you begin reaching out to attorneys, make sure to find one that specializes in M&A and corporate restructurings. Trust me, it’s worth the price. Without the requisite expertise, a lot of critical pieces can slip through the cracks and lead to utter disaster. But don’t fret about the billable rate just yet; there are a few independent lawyers who charge well below standard firm prices and provide excellent service.