David Einhorn, a hedge fund manager worth north of a billion dollars, isn’t bullish on technology stocks. In a letter to his investors sent today, Einhorn described the current market environment as the “second tech bubble in 15 years.”

Calling today an “echo of the previous tech bubble,” Einhorn notes that there are currently “fewer large capitalization stocks and much less public enthusiasm” this time around. This means that the current bubble, such as it is, is smaller, and when it does deflate — how rapidly we’ll have to see — there will be less carnage — blood, red ink, or otherwise.

It’s worth our time to walk through Einhorn’s arguments concerning tech stocks and accounting practices. Here are a few “indications” that demonstrate, according to Einhorn, that “we are pretty far along” in the current bubble:

Valuing companies not based on their current profitability, and reasonable expectations of their future profitability, but instead on their pure revenue growth or other metrics is considered mostly reasonable at the moment. If it weren’t, Box wouldn’t get to go public, and things like this would certainly not happen. Thinking simply, Einhorn’s first and third bullet points are linked tightly. If we used conventional, even traditional, methods of calculating the valuation of many technology companies today that sport valuations north of a $1 billion, there would need to be a large correction.

Einhorn expects things to settle down, making the following historical argument:

This is a pretty decent encapsulation of the mental shift in the market in a post-bubble environment. Once it gets a little harder to raise more money, you have to either have your own or make some more. Cash on hand and profits are, after all, the fuel and goal of business.

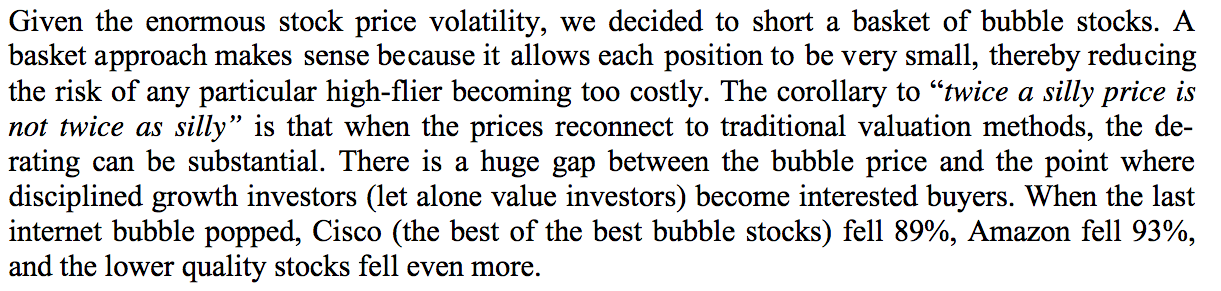

Einhorn thus thinks that many technology stocks are comically overvalued, so he’s shorting them:

What’s interesting is that Einhorn thinks that a cadre of companies out there are potentially so overvalued that they could lose 90% of their value:

Damn. I don’t disagree. The question is how long investors will be content to watch firms lose money in the name of revenue growth.

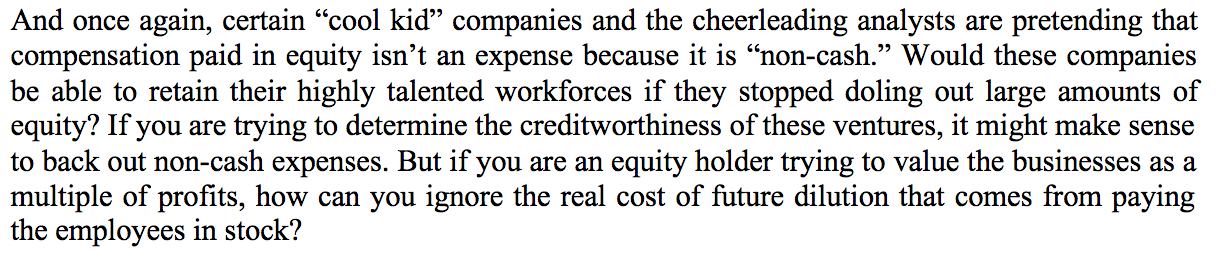

Finally, Einhorn isn’t impressed with your non-GAAP earnings that discount the cost of paying employees with stock in addition to cash. It’s trendy — perhaps it always has been — to report on cash-based expenses in adjusted earnings statements. Einhorn doesn’t like this:

At least in a long-term sense, this is very reasonable. It ties into the above points concerning valuation metrics: If we are discounting the cost of non-cash expenses in our valuing of emerging technology companies, we’re probably skewing more than a little.

Are we going to stop anytime soon? Probably not. As TechCrunch recently reported:

There is a reason it feels like everyone and anyone is raising money to build a company: They are. According to two studies, capital raised from venture capitalists by growing, private companies is at its highest point since 2001.

A study by MoneyTree pegs the total sum raised in the first quarter at $9.47 billion. By its number, that is the highest figure since the second quarter of 2001, when venture capital invested $11.5 billion. The year-ago quarter according to the study saw a more modest $6.01 billion of inflow.

A separate study by DJX VentureSource has a slightly different figure for the period, estimating total first quarter investment at $10.7 billion. It also estimates the comparative 2001 figure at $11.5 billion, however.

Keep in mind that venture capital spiked to more than $28 billion per quarter in the last bubble, so we are not utterly out of control. But I think that Einhorn does correctly call down parts of technology as overheated.

On the other hand, large technology companies — Amazon aside, as always — are valued modestly. Microsoft’s trailing price-earnings ratio is 14.81 and Apple’s is 13.22.

So, while we’re seeing elements of technology get slightly goofy, there is sanity to be found as well.

H/T to ValleyWag for bringing the letter to our attention.

IMAGE BY FLICKR USER Ben Watts UNDER CC BY 2.0 LICENSE (IMAGE HAS BEEN CROPPED)