Earlier this week, the IRS decided that Bitcoin is property, not currency, setting in place a regulatory structure that could see users of the cryptocurrency forced to keep price score in a rapidly shifting market.

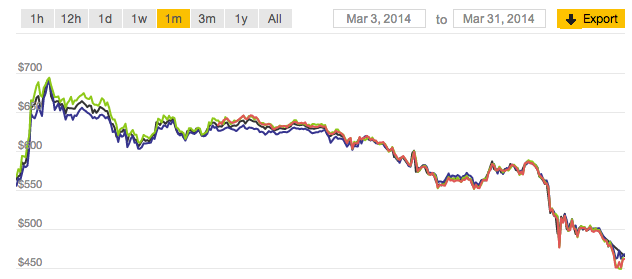

Bitcoin had a rough time of it last week, as GigaOm reported, losing around 17% of its value. Part of that was tied to a rumor regarding Bitcoin in China, and part, I think due to the IRS’s decision. Prices have continued to slip through the weekend.

Here’s a one month chart of Bitcoin, tracing four major exchanges:

What gives? If you are forced to treat Bitcoin as a property, you must take capital gains into account whenever you make a purchase (transaction) with the stuff. I can’t improve on Bloomberg’s take on the situation:

Purchasing a $2 cup of coffee with Bitcoins bought for $1 would trigger $1 in capital gains for the coffee drinker and $2 of gross income for the coffee shop.

So as the price of Bitcoin tracks up and down, the user of Bitcoin for transactions would incur ever-shifting capital gains or losses with each purchase. These would have to be tracked carefully, and weighed, to tally up the final year-end score for tax purposes. This cuts at the value of stored gains, implied or realized, given that the government either wants a slice in the future, or has already laid claim to one.

So when you see the current Bitcoin market cap, keep in mind that, at least in theory, a chunk of that belongs to Uncle Sam. (The vast majority of Bitcoin trades are executed in United States Dollars, implying heavy usage by United States citizens that fall under the purview of the IRS.)

The idea of reporting the result of your Bitcoin activity to your government, as you can imagine, is somewhat antithetical to the idea that Bitcoin works outside of the realm of state actors — how can it be unregulated if it is regulated?

Those who made vast dollar sums in 2013 as Bitcoin prices skyrocketed and are of United States’ citizenship have to decide whether to report the income and pay steep capital gains tax, or submit fraudulent tax returns. I doubt that many people who bought into Bitcoin for either fun or hope expected to have such a choice placed in front of them; are they prepared to find a way to track their precise dollar gains and report it properly?

Some are calling for startups to merely bake a tracking feature into their wallets to track the capital gains tax of their users. That’s fine, but again not really in keeping with the ethos of Bitcoin, as least as well as I understand it.

It’s worth keeping in mind that the bets being made on Bitcoin by technologists are predicated on the stuff becoming regulated enough that the United States government doesn’t become a foe — these are often US-based companies, after all. At the same time, if everything positive that is extra-technical is removed from Bitcoin — its pseudo-anonymity, its lack of government intrusion, etc — what Bitcoin is could be merely less than what had once been hoped for.

As a final thought, there are a host of cryptocurrencies that promise better technological underpinnings than Bitcoin. If they can best Bitcoin at its only game, what will keep Bitcoin’s value up? Its network remains an asset for the cryptocurrency. If that same growing network of buyers, sellers, holders, and traders can stop the sag in Bitcoin’s price, however, is a bet for investors to make.

ILLUSTRATION BY BRYCE DURBIN