Clinkle, a mobile payments startup that aims to put your entire wallet on your phone, has raised a $25 million round from over 18 investors.

The company, which has been in stealth mode since it launched in 2011, was the subject of much hype and speculation in April when a Wall Street Journal story explained that over a dozen students were leaving Stanford to launch the partially professor-funded startup.

Beta testers, a former employee, and even Clinkle’s website have given us a look at how the app will function and what it will look like. Here’s the run down on one of the most interesting – and mysterious – startups in the Valley.

The Funding

A funding round with this many participants has been referred to pejoratively as a “Party Round,” which some investors like Chris Dixon warn against.

Clinkle founder Lucas Duplan told me Clinkle took on so many investors because it was an “important thing for us to have a group of people together who have a broad set of experiences in a number of areas,” as the company faces a wide range of challenges in attempting to solve a big problem.

“This is not a small social app,” he said. “What we’re trying to do here is fundamentally change how people trade. Every human being, every day, has to do this.”

Duplan declined to comment on whether any of the investors would be joining Clinkle’s board, or on any of the fundraising timeline.

“I did not want to be distracted by press and the media,” Duplan said. “I decided it would be better to really focus on product and announce the round once everything came together and we were happy with where we were in the company’s evolution.”

Duplan said most of the money will go towards hiring. The company currently has around 50 employees, and will be “rapidly expanding.” Duplan said new hires will fill a range of roles, from engineering to marketing to design, and more as the young startup fights against much larger competitors.

The Idea

Duplan came up with the idea while studying abroad in London the summer after his freshman year. He was frustrated that he could download apps to do virtually anything abroad–call friends, stream music, even Scrabble with friends back in California–except pay for a sandwich.

The next summer, Duplan and about 10 other students rented a house in Palo Alto and began developing Clinkle.

“I think there’s a big disconnect between the hype and the reality on the ground,” Duplan said. “There is currently no serious contender to cash and cards.”

Duplan said faces two major hurdles: technology and adoption.

The Technology

Duplan said that there hasn’t been a scalable solution that enables a phone to pay a merchant without replacing the point of sale system. Duplan said Clinkle has figured out a way to make this happen without requiring infrastructure change.

Clinkle did a small beta test at Stanford that Duplan said “went incredibly well.”

Stuart Upfill-Brown graduated from Stanford earlier this month and was a beta tester for the app. He said he would pay other friends who were testing the app back for small things, like a late night pizza.

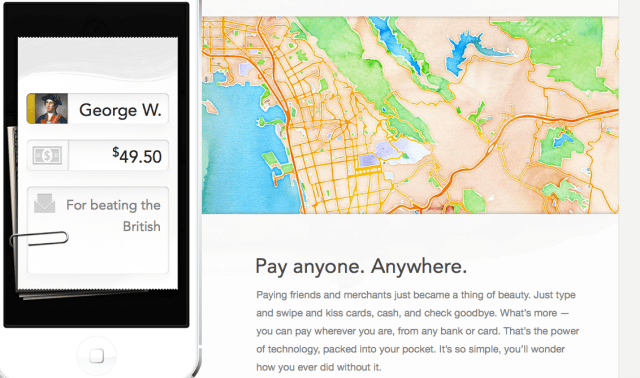

“It takes mobile banking to almost a social media level,” he said, explaining that you could pay friends back with stylish little notes and personalize your wallet.

“I thought the interface was intuitive because it’s designed to look like your wallet or a money clip would,” Danny Organ, another recent Stanford graduate and beta tester, said. “It’s nice to have everything in front of you visually.”

The two say the setup process was quick and simple: entering bank account information, setting a security code, and adding other friends who had the app. Clinkle uses a separate bank inside the app, called “Clinkle cash.” Users could transfer money back and forth from their bank accounts into “Clinkle cash.” These Clinkle dollars were then used for peer-to-peer and peer to merchant transactions.

“Anything that you would do with your wallet you would do now on your phone,” said a former employee who spoke on condition of anonymity. “That includes checks, credit cards, cash.”

Upfill-Brown used the app at campus mainstays like the Treehouse and Coho, where he would order and pay ahead of time through the app, and then go pick up his food.

“They very clearly are trying to put your whole wallet in your phone, whereas other things are covering one element. Clinkle felt more like ‘I can just leave my wallet at home,’” Upfill-Brown said.

Upfill-Brown, Organ, and the former employee all spoke to the usability and aesthetic design of the app.

“They’re a very driven company and they have a lot of talent,” the former employee said. “Their head designer, Rob Ryan, is the best asset of their company…that’s why it looks so good and functions so well.”

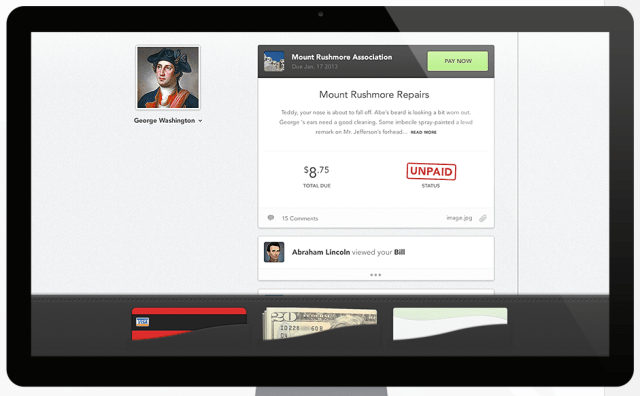

In addition to solo peer-to-peer transactions, Clinkle is adding group payments. There will be a messaging thread in the app where you can create groups and do group transactions.

Adoption

“Building great technology in a vacuum isn’t going to be very helpful,” Duplan said.

Referencing Facebook spreading via small collegiate networks, Duplan said the company wants to be smart and systematic in releasing the app.

“I think for something like a mobile wallet to be useful to people, you have to have ubiquity in acceptance,” he said, noting the gargantuan problem in getting every merchant to do the same thing.

“The best way to form a new network is to start with small, close-looped groups and expand slowly from there,” he said. He said Clinkle will be releasing to “a good number” of colleges and Universities in the next year. He declined to give a timeline on when the general public could get the app.

Duplan explains that starting at colleges makes the problem a lot more manageable, as there are lots of peer-to-peer payments and many of the peer to merchant payments are to the same few merchants–the campus pizza place, the grocery store, the nearest place with cheap, delicious Natty Light, etc.

Clinkle will launch at schools depending on the demand from the student body, which they will gauge via the online waiting lists. (Edit: I previously wrote that it will launch at any school that gets 1,750 students to enter their email address, in fact, this was just the number I was seeing on the website based on Stanford’s size and is not universal for every school)

Clinkle will launch at schools depending on the demand from the student body, which they will gauge via the online waiting lists. (Edit: I previously wrote that it will launch at any school that gets 1,750 students to enter their email address, in fact, this was just the number I was seeing on the website based on Stanford’s size and is not universal for every school)

The company has tossed around the idea of having a raffle-like contest to boost growth at colleges, where students get tickets for every invite the send out that leads to a sign up; rules and prizes, from wild trips to Clinkle swag, for the contest were on Clinkle’s website earlier this week. Now, Duplan tells me the company is rethinking the contest, along with other strategies for growth.

The former Clinkle employee said the company won’t take any fees on peer to peer transactions, and will look to monetize elsewhere, potentially taking small cuts from merchants if customers use Clinkle coupons or special offers. Duplan says Clinkle will take fees on peer to merchant transactions; while declining to give specifics, he says the fee will be “competitive” and will be paid by the merchant.

“It’s a lot easier to monetize payment than it is to monetize many other social apps or something else,” Duplan said. “When there’s real value being exchanged, there’s a ton on the line.”

The Verdict

The idea is a great one–I could not agree more with Duplan’s quote regarding current apps versus cash and cards. The app is beautiful and has positive reviews from early users. I’m a bit skeptical about the contest–essentially paying for growth–but it would be a small price to pay if they’re able to really take over the college market and spread from there.

Now they just need to get the app out there.

The former employee said he doesn’t know why they’ve taken so long to release the app, given that it works well in small beta groups, but assumes it’s related to the company’s growth strategy, not an engineering issue.

“They have the top engineers out of Stanford and they have a lot of them, and they’ve been working on it for a while,” he said.

“I think a lot of people at the company also have that same mentality,” the former employee said, regarding why it hasn’t launched yet.

Duplan said that in order for people to adopt Clinkle, the product must be an order of magnitude better than cash and cards.

“The margin for error is zero,” Duplan said.

Note: I removed two paragraphs from this post regarding Clinkle’s technology. While the information my sources gave me is accurate, it is far from a complete picture and, absent more detail, could be misleading to readers.