Kuapay, a startup offering a consumer mobile wallet application and accompanying loyalty platform for merchants, is rolling out an upgraded version of its mobile app today. The app focuses on improved speed, security and a new user interface that makes it easier for users to track their credit card details, as well as discover nearby local merchants that support the Kuapay service.

Based in Santa Monica, Calif., the company was founded in 2011 by Joaquin Ayuso de Paul, previously the co-founder of Tuenti, which sold to Telefonica for $100 million. The company uses an interesting combination of QR codes, barcodes, NFC or manual entry, any of which can be used at point-of-sale as an alternative to the credit card swipe. For security purposes, the app doesn’t actually transmit the credit card information between the phone and the register. Instead, the company integrates with POS systems like NCR, Micros, Aloha and others to complete the purchases.

Security is a big focus for the company, which PIN-protects its app and encrypts financial data in a Kuapay vault, which is also only accessible with device-specific, encrypted tokens. In the case of a lost device, users can remotely disable their accounts via the web, which would prevent anyone from using their credit card data, even if they could get past the PIN.

Around this time last year, Kuapay had 40 supporting merchants, mainly in the Santa Monica area. Today, it has grown its worldwide footprint to 600 locations. Instead of targeting the market region by region, however, Kuapay is spreading out in Europe, South America and Latin America, in addition to the U.S.

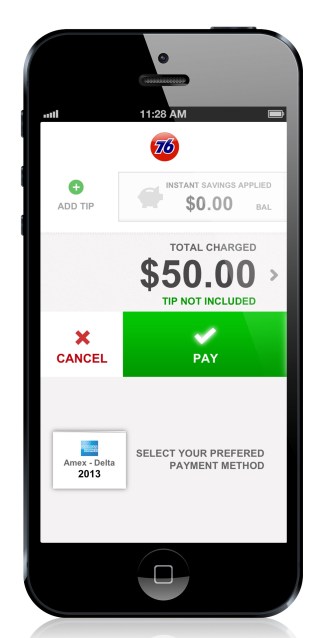

The company is running a pilot program with KFC here in the States, which includes trials in more than 100 KFC stores, a dozen of which are also testing a mobile ordering system that allows customers to pay ahead of their arrival at the store. It’s now piloting trials at two gas stations (76 Gas) which would allow drivers to pay without having to swipe their cards at the pump, too. And it has closed deals with several major retailers in Europe, including two large pizza delivery chains. Meanwhile, in Chile, it has moved into production mode with three banks and the national processor in the country. (The company has $4 million in funding from a single, private investor in Chile, it should be noted).

The company is running a pilot program with KFC here in the States, which includes trials in more than 100 KFC stores, a dozen of which are also testing a mobile ordering system that allows customers to pay ahead of their arrival at the store. It’s now piloting trials at two gas stations (76 Gas) which would allow drivers to pay without having to swipe their cards at the pump, too. And it has closed deals with several major retailers in Europe, including two large pizza delivery chains. Meanwhile, in Chile, it has moved into production mode with three banks and the national processor in the country. (The company has $4 million in funding from a single, private investor in Chile, it should be noted).

Stateside, Kuapay is being used in Santa Monica, L.A., San Francisco and New York, primarily with small businesses like dry cleaners, coffee shops and bookstores, for example. In the updated version of the application, users can now view all these merchants in their area and view their locations on the map, which is especially helpful in tracking food trucks using the service.

Though Kuapay has some significantly sized deals under its wing now, the company’s efforts in attacking a worldwide market instead of growing region by region may find it struggling to gain consumer awareness and adoption. Shoppers already have far too many alternative ways to pay on hand, including Square and its overseas clones, PayPal, Google Wallet, and NFC-based initiatives, such as U.S. carrier-backed Isis, plus mobile payments services from leading credit card companies and banks. None have yet to establish a significant traction at point-of-sale — consumers still just swipe their cards or pay with cash. The fragmented mobile payments market is due for consolidation, which means smaller players like Kuapay may either get swept up by larger firms, or find themselves in need of a new strategy.

On that front, Kuapay has another potential area of expertise it could fall back on, as it turns out. The company is supporting e-commerce transactions, too — in Europe with the pizza companies, but with a few major retailers here in the U.S., as well. De Paul says he’s not able to disclose which U.S. e-retailers are on board, saying only that the deals are “in the works” now and we’ll hear more about those soon.