Early-stage investor sentiment in India is mirroring the newfound caution we’re seeing on the West Coast this year, according to a survey from an Indian startup accelerator that runs a program in four different cities in the country.

GSF, or Global Superangels Forum, runs a nine-week incubator program in New Delhi, Mumbai, Chennai and Bangalore with five startups in each city. They surveyed 40 angel investors and venture capital firms in the country to get a sense of how firms are feeling about the market there. (The report is here.)

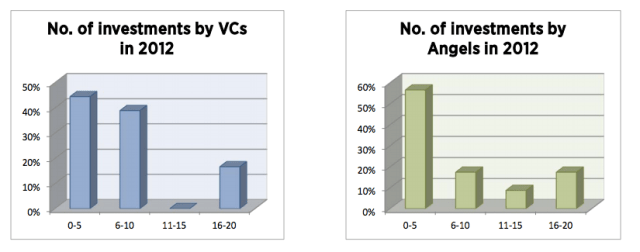

The study found that the pace of investments slowed. Most VC firms made fewer than 10 investments, while most angels in the survey closed fewer than five deals.

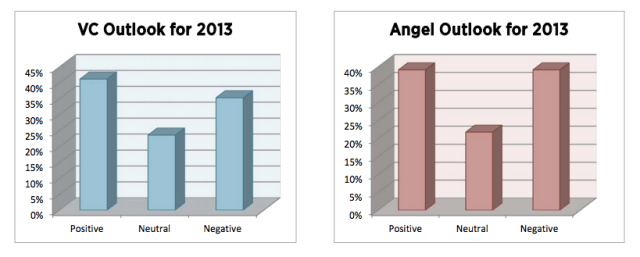

“I think we are certain to see a general slowdown in Series A investments in 2013,” said one angel who was unnamed in the study. “There will be a flight to higher quality, more complete and mature teams with a proven ability to build, scale and exit companies in 2013 as opposed to greenfield teams of very immature albeit talented founders.”

VCs are also doing more seed or angel-level deals — which also mirrors a trend we’re seeing the U.S. A few weeks ago, top Silicon Valley law firm Fenwick & West also put out a report saying that traditional venture investors are getting more active at the seed level. Not only that, they’re changing the character of funding deals, by moving them toward having a preferred stock structure instead of one that involves convertible debt.

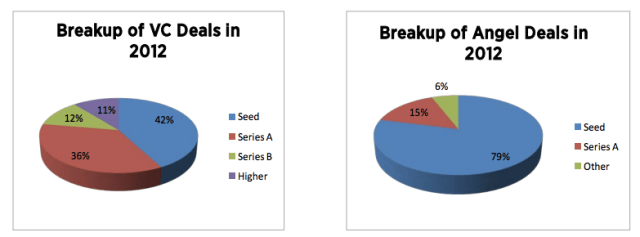

Similarly, in this GSF study, 61 percent of the Indian angels the firm interviewed said there was greater collaboration with VC firms last year than in 2011. The benefits are two-fold: VCs get exposure to more early-stage companies and get options to step up investment in them later on in a Series A or B rounds. At the same time, these VC firms may be better resourced to help these companies either find exits or scale their businesses.

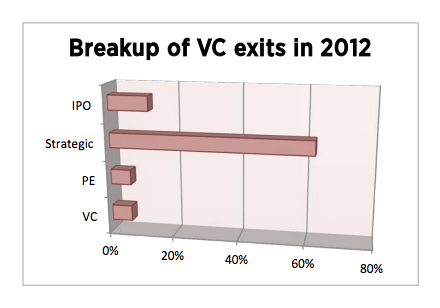

One area that both local Indian VC firms and angels find trouble with is the lack of exit opportunities for Indian startups. While the country has a hugely talented pool of technical talent, it hasn’t yet been able to translate that into a strong pipeline of IPO candidates. China in contrast has had a wealth of tech IPOs over the last several years, even though the market is in a bit of a lull after a frothy, overheated period. That’s partially because the Chinese government has chosen to create a “Great Firewall” and support domestic tech companies at the expense of foreign ones.

“They have their own Facebook. They have their own YouTube. They ring-fenced themselves,” said Rajesh Sawhney, who co-founded the accelerator. “That’s the not the situation with India. We’ve opened our doors. Our Google is your Google. Our Facebook is your Facebook.”

Indian consumer web and mobile startups have to compete on much more even footing with their U.S. and European counterparts, which can make it hard for domestic companies to break out.

At the same time, even though India has more than 1.2 billion people, its market is actually deceptively small given that there are fewer than 150 million people with fixed-line Internet access. But Sawhney is betting this will change in the next five years.

“We’ll add 1 billion new people from India alone to the web,” he said.