Wealthfront is one of my favorite startups out there today — because it has actually made me money. I’m not alone. The automated investments company has been growing its user base by 20 percent every month, because it cuts out traditional mutual funds and investment advisors and charges its users a very low fee for returns that have been beating the Street.

Now it’s aiming at the sluggish and shady finance industry with a $20 million second round of venture funding led by Mike Volpi of Index Ventures, Chamath Palihapitiya of The Social+Capital Partnership and Reid Hoffman of Greylock Partners — plus a large group of angel investors including Matt Mullenweg, Andy Dunn, Adam D’Angelo, Michael Schroepfer, Hunter Walk, Cipora Herman and Satya Patel.

My personal story is pretty typical of why the company has been doing so well.

After Inside Network got acquired in May of 2011 — and after I’d paid off all the taxes and a scary credit card debt from my previous, failed startup — I was stuck trying to figure out what to do with the money I had left. I talked to some financial advisors who recommended various packages that promised uninteresting returns, along with fees that looked to zero out any of those gains. I sat on the problem for months, unsure of what to do.

I’d seen Wealthfront launch at the end of 2011 and was curious (it was promising to solve my exact problem), but I only got around to trying it last November after it added an online wire transfer option that didn’t require me to spend hours filling out transfer papers at my bank. Well, and also, once I became confident enough in the direction of the U.S. and world economies that I thought investing would be worth it.

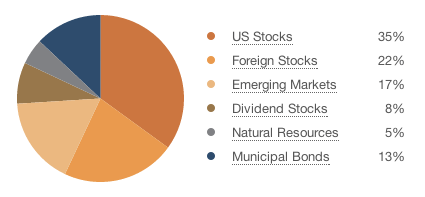

I went through its onboarding flow by directing its software to follow a conservative investment strategy fitting to my situation. Wealthfront picked mostly exchange-traded funds (ETFs) for U.S., foreign and emerging market stocks, along with bonds, real estate and natural resources.

I began making money from it immediately, no doubt benefiting from the particularly positive mood that many markets have been in since late last year.

By February I was like, hey this is pretty great, so I invested a smaller amount and directed Wealthfront to max out the risk on that account.

Today, nearly four months after starting to use the service, my conservative investment is up 4.4 percent and my risky one 5.2 percent. This might not look as good as the crazy numbers you see on benchmarks like the S&P 500, but as the company discusses here, it’s basically impossible to benchmark diversified portfolios like what Wealthfront offers.

Founder Andy Rachleff tells me that about a quarter of its users added additional money last month. And these people aren’t just 20- and 30-somethings like me who are fortunate enough to have the problem of investing hard-earned returns from their stints at successful startups.

Wealthfront has been growing through word of mouth, he says, as well as a rewards-type program for users who get their friends on board. About a third come through the latter mechanism. If you get somebody in, you get $5,000 of your money managed for free and they get $10,000 managed free. Note that Adam Nash, a top Silicon Valley product manager who joined after a great run at LinkedIn, is going to be focused on growth going forward.

In general, the company’s fees are set up to undermine the models of incumbent investment services like Fidelity, Schwab, and any other mutual fund investor or financial advisor. It charges a monthly rate based on an annual 0.25 percent fee, which compares quite favorably to the quotes I received from professionals — along the lines of 2.5 percent for a massive minimum required investment.

The low fees are only the beginning of what Wealthfront offers. Another feature is automated tax-loss harvesting for any account worth at least $100,000, which it added last year. If you make a profit on parts of that account’s portfolio, it’ll reinvest it and avoid taxes on the gains by doing so.

The company also sometimes makes larger changes to how it handles your money.

Earlier this month it adjusted all user portfolios to include a much broader range of bonds, as well as the addition of retirement accounts (allowing long-term investors to avoid yearly taxes). The expected gains from these changes, which were masterminded by the company’s legendary Chief Investment Officer Burt Markiel, come out to about 0.5 percent per year.

Where to now? Rachleff thinks he can carve out a solid chunk of the approximately $12.5 trillion individual investor industry in the U.S. A founding partner at top venture firm Benchmark beginning in 1995 and a Stanford Graduate School of Business lecturer since 2004, Rachleff is also a student of the real disruption going on here. He’s aiming for anyone who can’t afford the high requirements of most professional investors.

He says the company will be using the additional $20 million to invest in more improvements to the core product, as well as a major push for more growth.

The company previously raised a total of $10.5 million from a big group of angels, as well as DAG Ventures, beginning in 2008 when it began life as kaChing, which Rachleff described in an essay for us as being a not-so-disruptive social investing service.

[Update: There are competitors out there, that create a software layer on top of ETFs and other assets, that I haven’t used, and frankly hadn’t heard about despite looking around and despite some of them being covered extensively on TechCrunch (yes, our search features are weak). One of them is Betterment. There’s a nice debate between Wealthfront, Betterment, and various other competitors over on Quora. I’m personally going to try using Betterment as well and see how it works for me. I’m not taking back anything I said about Wealthfront, but I’ll do more posts on the issue as I try stuff out, and if you’re looking for options… read the Quora thread as a good primer.]