It’s so simple and disruptive I wonder why others haven’t really tried it. Droplet is a mobile money app on iOS that lets you load cash onto your phone and send payments to anyone – including participating retailers – for free, via email. Unlike mobile payment companies like Square, iZettle and apps from the banks who own Visa and Mastercard, Droplet is about digitising cash, not putting credit cards on your phone or carrying around a plastic card reader. But crucially there are no charges to the individual or the merchant. The idea behind droplet is utterly simple, but very powerful.

In Kenya, M-Pesa processes more than a quarter of the country’s GDP via mobile phones because there’s virtually no banking system. Droplet could well do the same, if it plays its cards right, and create a viral adoption loop. All it would take would be for retailers – especially small ones – to start promoting it themselves.

Right now it only works with merchants in Birmingham, UK, but there are plans to roll it out more widely. You can try it out here and use it across various shops bars and restaurants in the city for now.

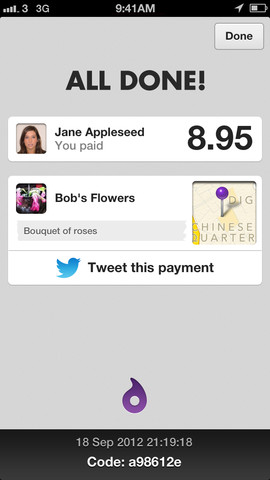

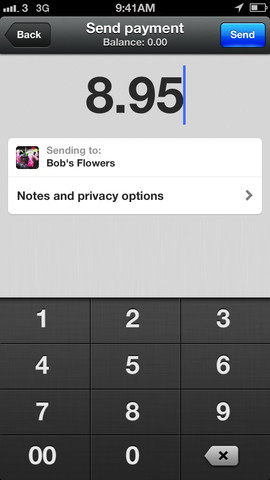

You and whoever you want to pay both have to have the app. But once you do, you can add cash to it via a debit or credit card (in multiples of £10) and pay anyone who both has the app and an email address which is associated with the app. You can also scan a special bar code with your phone when you reach the till of a retailer. Cleverly, the app itself shows nearby merchants based on your location, making it even easier to find the merchant you want to pay, assuming you are in the shop at the time. It also gives you the ability to add notes and search your transaction history – this could be very powerful. It’s not unlike Venmo which was acquired this year.

In theory you could use it for any currency, though right now it would be converted into Pounds Sterling.

Droplet is highly disruptive because the startup has decided not to charge anything to add money to your account, and it is also free for merchants. Merchants love it because it’s a way of avoiding bank charges and the extras that iZettle and others would charge.

The startup could well light the touch paper on something. It costs almost nothing to move information around the web, so why does the banking and payments industry still charge users to move their own money around? Exactly.

Co-founders Will Grant and Steffan Aquarone set out to create such an app after sitting in a coffee shop.

“We were sat in Urban Coffee Company in Birmingham and thought about all the things that hadn’t yet been transformed by the web. It was quite clear the banking and payments industry was ripe for disruption and the customer experience could be rebooted and simplified,” says Aquarone

The nine-strong team has put the app into beat for the last six weeks and has revealed its numbers from the trial to TechCrunch for the first time:

• 50+ merchants in Birmingham City Centre and counting

• 1,000+ users and growing

• Average top up value £17.89 and increasing

• Average payment value £10.68 and increasing

Here are some stats:

The security is, they claim, military-grade, and they spent a year prior to the beta launch ensuring the platform was extremely secure. “We’ve got all the security measures in place that you would expect from a global online bank. What’s more, we don’t store any sensitive information on people’s phone; it’s all on our secure servers, which use SSL/TLS encryption. There is no permanent connection to bank accounts either, making it even safer,” says Aquarone. Amongst the team is the former brand director for Visa Europe.

How will they make money? When people top up their accounts, Droplet holds their funds in trust. This means they can take their money back out of the Droplet economy at any time. But Droplet makes a very small amount of money in interest from these deposited funds, which covers the cost of the system. So far they’ve seen a very encouraging ‘dwell time,’ where instead of taking their money back out, people are leaving it in their Droplet accounts and sending it to other people – they are even starting to see the first B2B payments using Droplet.

Droplet also has backing from the E4F Accelerator on Birmingham Science Park.

Now, admittedly there is the threat of money laundering; however Aquarone says they have built a number of machine-learning tools into the system to detect odd behaviour like that.

But technically there is nothing to stop Droplet spreading virally if retailers and merchants decide they want to promote the app. Certainly, in these straightened economic times, you can see many hard-pressed small retailers jumping on something that avoids multiple bank charges.