Editor’s note: David Haber is an analyst at Spark Capital. Prior to Spark, David helped launch Locus Analytics, a start-up asset management business. Follow David on Twitter.

I spent the summer of 2007 working at an online education startup in San Francisco’s SOMA district called Batiq. It was the summer after my sophomore year in college and my first introduction to the world of startups and to a group of individuals – whether they realized it or not – that would dramatically alter the way I thought about business and technology.

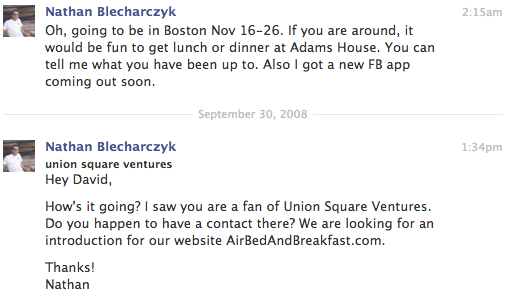

One of those people was a recent Harvard grad and our lead developer, Nathan Blecharczyk. We kept in touch over the next couple of years while I finished school and he moved on to his next project, “Air Bed and Breakfast.”

While I didn’t have a contact at USV at the time, I remember thinking that his business sounded neat, but that there couldn’t possibly be that many people who would want to share their home with strangers. Turns out I was in good company.

It wasn’t until the following summer while I was working for the founder of a pharmaceutical royalty company, Royalty Pharma, and watching Airbnb make waves during the Democratic National Convention, that I would fully grasp the potential of marketplaces. It made me internalize what “liquidity” was all about.

What became clear to me during this time is the immense opportunity to be the liquidity provider in a market (existing or new) where there are valuable assets (be they real estate or pharmaceutical royalties) that are, under the status quo, under-monetized.

With its infinite space, instant access and seamless connectivity, the Internet provides the perfect medium to aggregate the long tail of fragmented and illiquid markets. This dynamic has made the opportunity for creating online marketplaces so compelling.

My colleague Andrew Parker perfectly articulated this point in a blog post from 2010 in which he illustrated the “Spawn of Craiglist” and the impact that it had in the various markets it addressed. As Chris Dixon recently highlighted, some of these opportunities are so large that they require specific focus to be successful.

I thought it might be worth revisiting Andrew’s graphic, to see how the world has changed since 2010:

It’s safe to say that there has been an explosion in marketplace businesses. These 82 companies (nowhere near exhaustive) have collectively raised close to $2 billion in venture capital and have created many billions of dollars in value. As I look at this list, as well as all marketplace companies that we get pitched at Spark, I keep coming back to a few salient points that I believe dictate the potential value of these companies:

- Size of the Market. Don’t be fooled by the incumbent market. Think about the one that may be created or unlocked. While the initial focus might be small, what does the potentially broader market look like for this company (i.e. from couch surfing to the travel lodging industry in its entirety)?

- Excess Capacity. Some call it an asymptotic market, but it’s simply the fact that a good portion of a given industry is sitting idle or under-monetized. Why is that? Can it be changed by a new business?

- Friction/Opacity. Are there middlemen in this market that shouldn’t exist? The larger or more considered the transaction, the more likely there are intermediaries (i.e. buying a bike vs. buying a company). Intermediaries benefit from (and often perpetuate) opaque markets. They withhold information in order to make margin. Value is created when these intermediaries can be dis-intermediated.

- Fragmentation. Is this market highly fragmented, or are there a few dominant players? There isn’t much opportunity in a market where there is concentration on one side or the other.

- Customer Experience. Whether you become the transaction processor that eliminates an awkward in-person cash transaction or simply provide a more compelling user interface to a staid business (i.e. like Uber has done with the livery business), a better customer experience can be the differentiating factor for your success (and one that keeps transactions within your platform).

While these are interrelated points (and there are certainly others that I have missed), these are the ones I often come back to. If you look back at the graphic above, the most successful companies to date have addressed these issues.

While the talk of the Internet town these days is that the wind behind consumer Internet companies has waned, I still fundamentally believe that there are opportunities for businesses to provide liquidity to large, previously untapped markets. I’m especially keen to see mobile-first approaches to marketplace businesses. And I also expect many of these marketplace dynamics we’ve seen in consumer businesses to emerge as key elements in the next generation of successful b2b and enterprise software businesses. We’ll be looking for these.