ModoPayments’ simple and comprehensive solution for providing mobile payments is interesting and what’s more, its offer-based approach may have finally cracked the code for monetizing check-ins. This is something that mobile location-based service providers (LBSs) like Foursquare, Loopt, Gowalla and ShopKick have, no doubt, been laboring over since their inceptions. And while ModoPayments is, at present, a non-NFC mobile payments platform, they plan to integrate with NFC too, when NFC reaches retail maturity.

Based in Dallas, Texas and led by CEO Bruce Parker, ModoPayments is a startup with a goal to do exactly what their tagline says – “convert redemptions to payments and make payments mobile”. What exactly does that mean? First, know that ModoPayments definitely has a payments piece and I’ll come to that in a moment, but a supremely important part of their business plan is creating and tying value offers to the purchases they enable in order to enhance and promote their mobile payments solution. They create monetary savings that users can cash in on if they transact with ModoPayments instead of another tender.

It has often been stated that mobile payments are a solution searching for a problem. Indeed, what is the big deal about pulling a card out of your wallet vs. pulling your phone out of your pocket, to transact? Where is the value to drive the mobile payment other than convenience?

Modo thinks it has to do with offers and they have integrated a framework for redeeming merchant offers with their payments platform. This makes sense to me. If I had to choose between paying with my Visa card in my wallet or my Visa on my phone (that also happens to give me a big discount on the purchase) I think the choice is obvious. So right out of the gate, ModoPayments has tied a distinct consumer value proposition to their service in order to drive usage (they hope). Google Wallet has a similar concept. It will definitely be a motivator.

The platform makes it possible to, in the words of Bruce, “generate a mobile payment transaction at any location that accepts either Visa or MasterCard with no change to POS and no change to the phone that uses ModoPayments.” It can exist as an SMS or native app solution; customers can choose either touchpoint.

I’ve heard this one before, but their scenario is really simple and honestly sounds like it might work.

HOW DOES IT WORK?

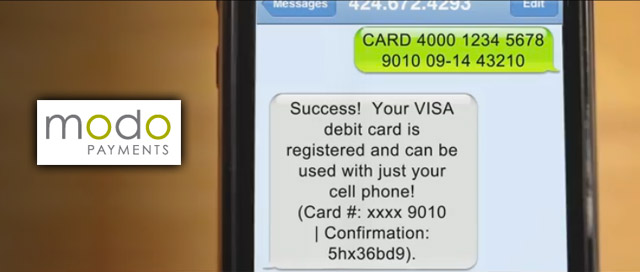

First, a customer creates an account at the ModoPayments website and registers a credit card with that account. When it later comes time to pay for something at a participating location, the customer texts “VISIT” to the Modo short code or else they check-in with the Modo native app. (In the text scenario, Modo will try to triangulate on a customer’s network location. If they can’t locate them, ultimately they will just ask the customer via text—‘are you at X location’ and via process of elimination, locate them).

After Modo have verified that the location matches up with a supporting offer, they will create a randomized credit account number for that location which is good for one transaction only. They then load it with money that the merchant or other 3rd party has set aside for the specific offer.

Next, they will grab the difference still needed to complete the sale from the customers registered credit card. In essence, they are creating pre-paid card numbers that will only work for a limited time and that are loaded with money from both the offer provider and the customer.

Then, they send half of the account number to the merchant and half of the number to the customer. The two sides combine their numbers to create the actionable account number to complete the transaction. (The merchant half of the number may or may not be static and therefore might not even need to be sent).

Pretty tricky. So here they have tied a distinct merchant value proposition to their service—no costly POS change required plus a mobile marketing channel.

SHOW ME THE MONEY

Logistically, that is how they are enabling the mobile payment but another concept they are focused on is information sharing. Using the ModoPayments framework, users can track their entire purchase history, merchants can see anonymized purchasing trends to track/create effective offers and the location element will act as a security feature and help bolster the ability to relax chargeback percentages in order to turn those into profit.

For example, normally for “card-not-present” credit transactions (like Modo’s) an extra percentage is taken from the merchant who accepts these card-less numbers as protection against fraudulent purchases in case there is a chargeback.

Because ModoPayments has these sophisticated technologies that can prove exactly where a transaction is happening and by whom, and because they also control the randomized account numbers they can potentially minimize chargeback risk. This will allow them to work out acquirer relationships in such a way that they keep that usual 1% markup and turn it into profit. I am not sure how they are going to pull that off, but it’s a great idea.

MONETIZE CHECK-IN

I think the payments piece alone is cool and the info sharing piece is borderline scary but what I really zeroed in on is what this could mean as a payments solution that benefits the check-in concept. Customers can check-in with ModoPayments via text or native app, but Bruce said that other LBSs could also own the check-in part if they want. Modo is open to that.

So here’s the thing…if pulled off correctly, this service could finally monetize check-in in a way that hasn’t happened before. Modo could provide the framework for the offer and mechanism for transacting, while the location service could act as the visible marketing channel. That extra 1% could be sliced up a few ways so everyone could get a piece of the action. Then, it just becomes a volume game.

For example, a merchant has an offer and advertises that either directly though ModoPayments or within say, Foursquare. If the Foursquare check-in helps drive the offer redemption through ModoPayments, then they get a piece of that transaction, affiliate-style. It would therefore behoove Foursquare to help advertise it. This could be the part of their puzzle that has been missing and could be very attractive to the major LBSs while at the same time could help to drive ModoPayments adoption.

WHAT ABOUT NFC?

I’m rather pessimistic about NFC’s short term viability for completing mobile payments in the retail space. No doubt it will be a useful mechanism once the merchant value proposition is defined. As it stands, that has yet to be clarified for me, in toto.

Sure, consumers want it, but is that enough of a reason to validate merchant expense incurred purchasing and installing the hardware needed, just so a small percentage of early adopter consumers can leave their wallets at home? Consumer desire is one thing but there needs to be a clear, strategic and financial value for the merchant too, especially if they are footing the bill for NFC enablement (e.g. buying hardware).

It’s a big, credible expense and there are just too many unanswered questions in my mind to think that NFC payments are as close as the Google Wallet announcement would lead some to believe. Forrester’s Charles S. Golvin and Thomas Husson have said that

“Relying on an installed base of phones that is today indistinguishable from zero, a single payment system, a single card issuer, and a modest network of merchants capable of accepting these phone-based payments means that the near-term impact will be negligible.”

That’s why the POS-less concept ModoPayments has put together is a great interim step.

Don’t get me wrong, I think eventually NFC will embed and payments solutions will have to incorporate with it and account for it. It’s definitely one way to solve for the physical proximity needs of a mobile transaction. It’s still a couple of years away though. That’s just my opinion.

And really, I’m not sure consumers care if their mobile payments solution incorporates NFC, 2D barcodes or a freakin’ chip in their butt…they just want an easy way to purchase that matches the evolving mobile lifestyle of traveling light, planning on the fly and managing on the go. It’s just how people are staring to do things. We all know this.

Ok, they might actually care about a chip in their butt. You get my point though.

WHAT’S NEXT

ModoPayments has a few pilots scheduled to launch in Dallas in the coming weeks, so we’ll hopefully be able to get a look at how this concept is playing out in the real world. I will definitely be watching for when and how those pilots work out. They will also be presenting at Finovate 2011, in New York later in September. Until then, check out their light and clever little video at modopayments.com.