C$ cMoney, a mobile payments startup based in Houston, is having quite a week. On Friday, the company announced an impressive funding round of $100 million from private equity firm AGS Capital Group. In total, cMoney has secured $115 million in funding commitments from AGS and a NY-based firm called Kodiak Capital Group.

C$ cMoney, a mobile payments startup based in Houston, is having quite a week. On Friday, the company announced an impressive funding round of $100 million from private equity firm AGS Capital Group. In total, cMoney has secured $115 million in funding commitments from AGS and a NY-based firm called Kodiak Capital Group.

The latest announcement was picked up by a few news outlets, including the WSJ’s Venture Capital Dispatch which touted cMoney as “a start-up with a funky name [that] has an ambitious plan for replacing consumers’ debit and credit cards with a mobile-payment system.”

Sounds like another promising company in the red-hot mobile payments sector—a market that Nokia, PayPal, and a host of startups like Zong are trying to crack. Except, I don’t buy it. There is too much hype, and too little actual product coming from cmoney.

That highly-touted $100 million funding, for instance, turns out not be a venture round at all, but rather an equity line of credit (a lot more on that later). And the company is being sued by a CEO it recruited. Read on for a tale of a bizarre reverse merger, promises of million-dollar fees, and a young, 28-year old founder who lists among her accomplishments and qualifications her childhood sports activities, including “dance, gymnastics, soccer, softball and tennis.”

What is cMoney?

The company, which launched in March 2009, is developing a mobile application that will let users send or receive money via temporary connections. According to reports, the application will be linked to a users’ credit cards and accounts. When s/he wants to make a purchase, the user logs-in to the app, submits information on the transaction, punches in a password and retrieves a code. The user will be able to give that code to a cashier for payment and after 15 minutes the code will expire.

Like many startups, the company’s product is not ready for market, it’s in the “demonstration” phase. However, cMoney has struggled to meet its own deadlines. According to an April press release the launch was scheduled for this summer, then a May SEC filing predicted a fall release, and now, in its latest press release, the company is predicting a 2011 launch.

Beyond the delays, the structure of the startup itself, is odd: cMoney acquired a company called Bonfire in May 2010 in a reverse merger transaction. According to an S-1 filing, Bonfire had no active operations and was previously a business based on “producing, marketing and selling audio recordings of folk tales, fairy tales and other children’s stories under the brand name ‘Bonfire Tales.’”

Bonfire also disclosed in late March, just before the merger, that it had “no cash and a working capital deficit of $28,845.”

In fact, there was only one employee, the director, Tim DeHerrera, who was scheduled to resign after the deal.

Unless cMoney wanted to tap Bonfire’s rich trove of children’s fairytales, why would a mobile payments company purchase a seemingly defunct company with only debt, no synergies and virtually no employees? The only real interest here, seems to be Bonfire’s status as a publicly traded company, trading over the counter as a penny stock (under ticker symbol PINK:BNFR). Reverse mergers are typically done by companies who cannot go public in a more straightforward fashion.

The Case Of The Missing CEO

On May 6, 2010, cMoney named Lawrence Krasner to the position of CEO, Krasner is a fairly seasoned veteran of Wall Street, as a former Senior Vice President of Lehman Brothers, a Senior Manager of Ernst & Young, and a VP of JPMorgan. Sounds like a solid coup for a fledgling startup, except Krasner never spent a single day as cMoney’s CEO, according to the company’s SEC filing.

Instead, Krasner is building a legal case against the company, suing them for damages in excess of $700,000 and 1,950,000 in fully vested shares of the company’s common stock, according to a filing. I reached out to Krasner on Friday, but he said he could not comment at the time. The company says the claims “are without merit.”

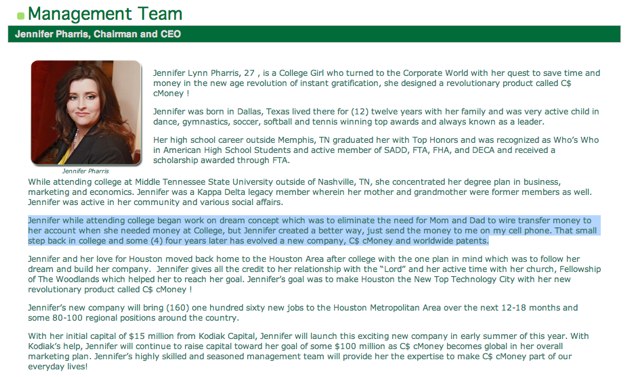

The founder of the company, Jennifer Pharris, has assumed the role of CEO and Chairman of cMoney. With the exception of a thin LinkedIn profile and her official bio on cMoney’s website, there’s very little information available on Pharris online. However, that official bio is worth a read— if you can make it through the syntactical quagmire:

Jennifer Lynn Pharris, 27 , is a College Girl who turned to the Corporate World with her quest to save time and money in the new age revolution of instant gratification, she designed a revolutionary product called C$ cMoney !

Jennifer was born in Dallas, Texas lived there for (12) twelve years with her family and was very active child in dance, gymnastics, soccer, softball and tennis winning top awards and always known as a leader.

Her high school career outside Memphis, TN graduated her with Top Honors and was recognized as Who’s Who in American High School Students and active member of SADD, FTA, FHA, and DECA and received a scholarship awarded through FTA.While attending college at Middle Tennessee State University outside of Nashville, TN, she concentrated her degree plan in business, marketing and economics. Jennifer was a Kappa Delta legacy member wherein her mother and grandmother were former members as well. Jennifer was active in her community and various social affairs.

Jennifer while attending college began work on dream concept which was to eliminate the need for Mom and Dad to wire transfer money to her account when she needed money at College, but Jennifer created a better way, just send the money to me on my cell phone. That small step back in college and some (4) four years later has evolved a new company, C$ cMoney and worldwide patents.

Jennifer and her love for Houston moved back home to the Houston Area after college with the one plan in mind which was to follow her dream and build her company. Jennifer gives all the credit to her relationship with the “Lord” and her active time with her church, Fellowship of The Woodlands which helped her to reach her goal. Jennifer’s goal was to make Houston the New Top Technology City with her new revolutionary product called C$ cMoney !

Highlights include the random capitalization of words like “College Girl,” “Mom” and “Corporate World,” and my favorite (for its casual, mid-sentence transition from the third to the first person):

Jennifer while attending college began work on dream concept which was to eliminate the need for Mom and Dad to wire transfer money to her account when she needed money at College, but Jennifer created a better way, just send the money to me on my cell phone.

In fact there are typos and run-on sentences all over the website, with words like “trough” and “prividing” popping up on the investor relations and FAQ pages. While it is a bit unfair to judge them in this manner, this is supposed to be a startup valued north of $115 million. It’s hard to comprehend how any investor would look at this website and agree to plunk down $100 million— or even a million dollars. Which brings us to that $100 million question.

Why did AGS and Kodiak Capital Group invest in cMoney?

At the time of this post, the firms had not responded to my requests for comment. With no ready-for-market product, six employees, a poorly managed website, a lawsuit from an almost-CEO, and apparently more than $2.5 million in accumulated losses on the books and just $47,831 cash on hand (according to an S-1 May 27th filing), cMoney doesn’t seem like a prime candidate for a $100 million cash infusion.

Then again, cMoney may not see a lot of that cash after all.

AGS’s funding committment is contingent on several conditions and the structure of the deal itself is bizarre. Under the agreement, cMoney has the right to compel AGS to purchase its common stock shares, to “put” shares to AGS. Depending on the price of the share at the time, AGS will get a discount— for example, cMoney is currently trading at 3 cents a share, AGS would be eligible for a 50% discount to 1.5 cents a share. However, the key part in this agreement, is that cMoney “can not put shares to AGS if such put would cause AGS to own in excess of 4.99% of our outstanding shares of common stock.” In other words, once AGS hits that 4.99% bar, cMoney can no longer compel them to purchase the common stock and with the company currently trading at a market cap of $1.36 million — AGS is only on the hook for maybe a couple hundred thousand dollars. Of course, AGS could elect to buy more shares, but I’m going to make a bold prediction here that the final investment will be laughable compared to the promise of $100 million.

Here’s the pertinent excerpt from cMoney’s July 7th filing:

On July 7, 2010, the Corporation has entered into a Reserve Equity Financing Agreement (the “AGS Equity Line of Credit”) and Registration Rights Agreement with AGS Capital Group, LLC. (“AGS”). Pursuant to the AGS Equity Line of Credit, we have the right to “put” to AGS (the “AGS Put Right”) up to $100 million in shares of our common stock (i.e., we can compel AGS to purchase our common stock at a pre-determined formula) for a purchase price equal to from 50% to 95% of the lowest closing bid price of our common stock during the five consecutive trading days immediately following the date of our notice to AGS of our election to put shares pursuant to the AGS Equity Line of Credit. That percent discount is: 50% if the price of our common stock is less than $0.11 per share, 25% if the price of our common stock is between $0.11 and $0.19, 85% if the price of our common stock is between $0.20 and $0.74 per share, 10% if the price of our common stock is between $0.75 and $0.99 per share, and 5% the price of our common stock is above $1.00 per share. The maximum dollar value that we will be permitted to put at any one time will be, at our option, either: (a) $100,000 or (b) 250% of the product of the average daily volume in the U.S. market of our common stock for the ten (10) trading days prior to the notice of our put, multiplied by the average of the ten (10) daily closing bid prices immediately preceding the date of the put notice. However, we must withdraw our put if the lowest closing bid price of our common stock during the five consecutive trading days immediately following the date of our notice to AGS of our election to put shares pursuant to the AGS Equity Line of Credit is less than 98% of the average closing price of our common stock for the ten trading days prior to the date of such notice. We can not put shares to AGS if such put would cause AGS to own in excess of 4.99% of our outstanding shares of common stock.

And why does a young startup, with such a small staff, need a huge cash infusion? It’s unclear how the money will be used to build the actual mobile application, but at the very least, we know they are spending a large chunk of change on salaries for the executive team. The chief operating officer, chief marketing officer and chief financial officer have a base salary of $250K per year, the chief technology officer is promised $215K.

Meanwhile, cMoney directly pays Pharris $500 a week, but (and here is where it gets interesting) her other company Global 1— which is not mentioned in her profile—receives $41,543 per year for 5 years of management services. As explained in a recent filing, these “management services are expect to be provided by Ms. Harris.”

More significantly, in April of this year, cMoney entered into a “technology license agreement with Global 1 Enterprises, Inc. Under the agreement, C$ cMoney will pay Global 1 $1,500,000 per year for an exclusive and non-transferable license to certain intellectual property included trademarks and patents. Global 1 is owned by Jennifer Pharris.” Thus, to spell it out slowly, Pharris is charging cMoney hefty fees for the rights to license the technology from her other company. It’s hard to estimate what her cut is from this deal, but I imagine it’s a substantial amount (there was no reference online of any other executives at Global 1). For a company that is still bleeding cash, it’s strange for Pharris to charge such a high premium to access technology.

Who knows, cMoney could have a brillant project underneath the jumble, but at the very least, this strange constellation of facts and questions paints a dubious picture. I have asked several people in the mobile payments space, including those who cover the sector for investment firms, whether they have heard ever of cMoney or AGS— no one said yes. As always, buyer beware.