A decade ago, tech IPOs ruled the stock markets and Silicon Valley. They were the end-all and be-all for ambitious entrepreneurs and venture capitalists looking to become instant billionaires, or at least millionaires. That was many booms and busts ago. The IPO market never came back, and the multiple financial meltdowns which brought on Sarbanes-Oxley and other regulations made going public even less appealing to shoot-from-the-hip entrepreneurs. The founders of the most successful tech companies today—Facebook, Skype, LinkedIn—are pushing off the inevitable IPO for as long as possible. And for smaller tech companies, IPOs seem hardly worth the bother.

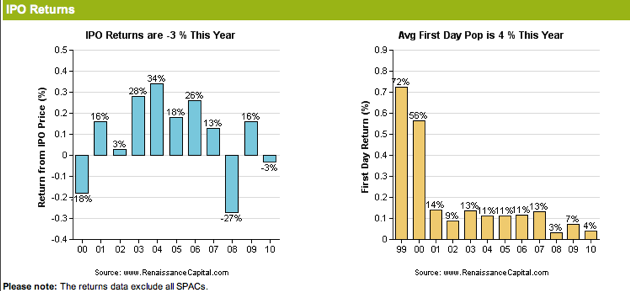

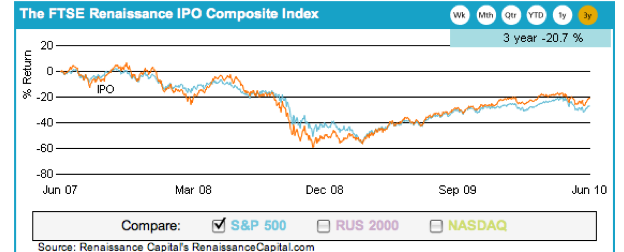

And those companies which are going public simply are not the cream of the crop. IPO returns across all sectors this year are down 3 percent, according to Renaissance Capital. And over the past three years, IPO returns are basically tracking the S&P 500, which hardly justifies the added risk of investing in them.

Even venture capitalists are souring on IPOs. In a post this morning titled “IPOs Just Aren’t What They Used To Be,” Fred Wilson laments:

The cost is just too high and the benefits are just too low for most companies these days.

Wilson shares two anecdotes. One was of a startup which prepared to go public, but couldn’t and was still stuck with a $3.5 million bill it couldn’t afford. The other was of a “successful” tech IPO which raised $75 million, but gave the company a lower valuation than it might have gotten in a “late stage private financing.” (He doesn’t name either company). In his opinion, “only the very best companies” should attempt an IPO: The exit of choice for most startups, he suggests, is selling to a larger company.

And that describes exactly the market today, where the best possible exit for most startups is to be acquired by Google, Microsoft, or (more recently) Apple. And instead of going public, the best tech startups like Facebook, Zynga, and Groupn are getting early payouts for founders and employees via late-stage, private DST-type financings.

But limiting exits to M&A might not be the best thing for venture returns. At TechCrunch Disrupt, technology banker Frank Quattrone argued: “For the VC market to produce above average returns you need there to be an IPO market.” An important part of venture returns come from holding onto some shares after an IPO and riding the public markets a while. “If you lose those longtail returns you lose a lot of the returns,” he concluded.

Quattrone seems to think this problem will be solved when the new standard bearers of the Web decide to go public, as opposed to the lackluster offerings so far:

There are probably 40 to 45 IPOs on file. They are not the category-defining, earthshaking companies the market wants to see. The market wants to see Facebook, Twitter, Zynga, LinkedIn, Skype. They want to see the companies that are changing the way we live.

I’m not sure a few iconic IPOs will bring back the Netscape years. First of all, it might still be a couple years before we see a Facebook IPO, and even longer for a Twitter IPO. But even if and when those kinds of tech companies do go public, the IPO option for lesser startups will remain limited for the reasons Wilson outlines. Unless, of course, a Facebook IPO makes public investors irrational once again and we get another bubble. But nobody wants that, or do they?