When 21-year-old college students Nate Matherson and Matt Lenhard started their first business for tutors, they didn’t really know that they would soon embark on a journey to help solve the $1.2 trillion student loan problem in the U.S.

Launched out of their University of Delaware dorm room, their first business was designed to help college tutors. The two even made it into an accelerator program in Cedar Rapids, Iowa, to work on the idea (if that doesn’t show the depth of their commitment, nothing will).

Cedar Rapids isn’t known for its bustling startup scene, but thanks to the Iowa Startup Accelerator and Built By Iowa, the two collegians were able to realize a few things.

One. Their first idea was a bust. Two. They were sitting on a potential goldmine in trying to solve one of their own problems.

Co-founder Matherson was saddled with roughly $50,000 in student loan debt. He had initially financed it with a few types of loans, but was now looking to refinance. It was then that he and his co-founder Lenhard hit on a potential business that was right under their noses.

The refinancing process for student loans is just too damn hard.

Normally, anyone looking to refinance their student loans has to fill out a fairly lengthy application each time they want to receive a loan. Their idea was — quite simply — to get rid of that hassle.

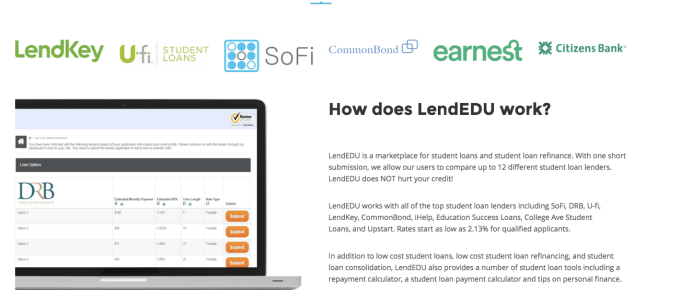

LendEDU is the fruit of their year-long sojourn in the entrepreneurial wild. A marketplace for student loan refinancing, the company’s service is simple. One application gets you visibility into all of the many different options for student loan refinancing.

The company calls it the Kayak of student lending. Average users at LendEDU save roughly $12,000 by refinancing their student loan debt (that’s a lot of beer, pizza, and ramen, y’all).

It also works with some of the biggest new student loan refinancing companies.

Right now, the student loan business is a big one. Seven out of 10 college grads matriculate with at least $29,000 in debt, and the $1.2 trillion overhang I mentioned earlier is a huge weight on the economy (and on the youngest members of the would-be-employed on who have to carry the weight of that debt).

What’s even more appealing about the service, the company says, is that it doesn’t hurt the credit of wannabe borrowers. The service is free for users and relies on what Matherson calls a “soft” credit inquiry, which doesn’t hurt an applicant’s credit rating.

Currently in the most recent batch of Y Combinator, the company has racked up some impressive numbers. They had 70,000 unique visitors to their website in January alone and have big plans for the coming year.

Matherson says that eventually the company will launch its own student loan marketplace (coming in April) and is working on credit cards that should roll out in the April timeframe, as well.

The idea makes a lot of sense. If a company already has the attention of a new set of borrowers right when they’re leaving school and entering the job market, it has a lot of insight into those borrowers’ credit history, payment habits, and everything else. Leveraging that to be a lender to this new generation is an easy route to customer acquisition.