Boku — the U.S.-based startup that enables consumers to pay for goods on their phones by charging directly on to their phone bills or deducting from available phone credits — is today announcing it is acquiring Germany-based Mopay, one of its biggest competitors.

The companies are not disclosing the financial terms of the purchase — we are still trying to find out and will update if we learn the price — but it is a big deal in another sense. Boku’s CEO Jon Prideaux says that the combined company becomes the world’s largest carrier billing provider, both in terms of carriers and content companies (and therefore customers) that will be plugged into the system; and in terms of the money that is getting processed as a result.

“By our estimates, Mopay would have been the second largest carrier billing player after us, so this is about combining the number two and number one players, which will help us make deals with large corporates and get the scale and take carrier billing to more verticals,” he said in an interview.

Prideaux would not disclose exactly what this means in terms of size except to note that the combined company will cover more than 5 billion mobile users in 80 countries and will add a “material uplift” to Boku’s revenues, increasing the number of transactions on the platform by two-thirds and more than doubling the customer base.

It will bring together content companies like Valve, gameloft, and Wargaming (from Mopay) together with Facebook, Sony, Spotify, and Electronic Arts (from Boku’s existing client base). Integration of their systems is starting now and Boku expects the two respective businesses to be sitting on a single platform by the end of 2015.

“This is a merger from strength. Both companies have strong growth plans, but felt that our customers would be best served by coming together to build a market leading mobile payments platform,” Mopay CEO Ingo Lippert said in a statement.

This is Boku’s second acquisition, after the company last year picked up Qubecell to expand its services in India and wider Asia as well as the Middle East.

Both Qubecell and Mopay are making good use of Boku’s significant venture backing. Since 2009 the company has raised $75 million, with investors including Andreessen Horowitz, Benchmark Capital, DAG Ventures, Index Ventures, Khosla Ventures, New Enterprise Associates (NEA) and Telefónica. Prideaux says the company is currently not looking for more funding.

While there is carrier billing available in regions like Europe and the U.S., companies offering such services are largely focused on developing markets these days.

The reason for this is because smartphone usage is booming in these markets, growing at a much faster pace than more saturated, mature countries. But credit card penetration is very low in emerging markets. That means consumers there are less likely to have credit cards to pay for things online, so carrier billing becomes a way for them to charge.

When discussing how a combined Boku/Mopay would look, Prideaux focused on how the two match up in these kinds of markets. Both companies are in China, he tells me, but with different partners. Meanwhile, Boku is strong in Singapore and India, while Mopay has gained more ground in Indonesia and Vietnam, he says. Emerging markets have also been the main target of late for one of Boku’s other big competitors, Bango.

The other big trend in carrier billing is in terms of what kind of goods get charged.

Today, Prideaux says that virtual goods (through mobile games) “remain the mainstay of carrier billing purchases.” (That’s a purchasing trend, along with dating, underscored through research by Mopay itself.)

These are also the smallest kinds of transactions you can have on mobile, with tiny margins for the parties involved in enabling them — hence the push for more scale and consolidation among those who power carrier billing services. Without strong margins, aggregation at least provides a better volume of business.

Going forward, Boku has been working on going up the food chain and “extending carrier billing to the digital segment.” In other words, more digital content around areas like music — where Boku already provides billing for companies like Spotify. Here it’s also about sweetening the deal by offering a way around the marginal cost that a merchant might have were it to take credit cards instead. “The market for digital content is five times as big,” Prideaux says with some optimism.

The even longer term prize is to extend carrier billing to be used for all kinds of goods. Boku is already working on this as well, having signed a deal last week with the three major carriers in the UK — O2, EE and Vodafone — to power e-money purchases, covering not just physical goods but also things like bus tickets. Right now, he tells me, the limits for carrier billing purchases are around the $50 mark on average in markets where this has been enabled.

But for now there is still a lot of work to be done still even in that first charging category: that of virtual goods and other in-app purchases.

It was only last month that Amazon turned on its very first carrier billing services for its appstore (in Germany as its first test market) — nearly two years after first announcing that it would do so.

Meanwhile, while you can buy virtual goods on the Windows Phone store and Google Play, there is one very app store operator noticeably absent from the mix.

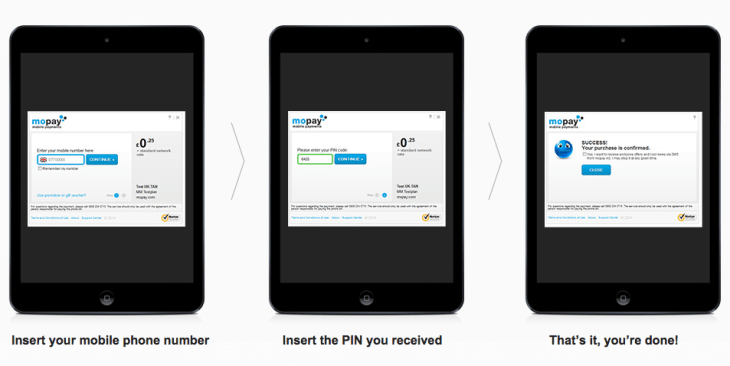

Although there has been speculation about whether iPhone and iPad maker Apple would ever allow carrier billing for its App Store, the company has yet to even make so much as an announcement or even offhanded reference about where it stands on the subject, even if we have heard behind the scenes that there is indeed something in the works, slow as it may be to reach the light of day. (The screenshot above is from a mobile web site.)

But as Apple — like other handset makers — looks increasingly at markets like China and other developing economies to grow its business, it’s bound to consider it as a way of bypassing the lack of credit card penetration, regardless of how card-based Apple Pay appears today.