In the world of personal finance, robo-advisers like Betterment, Wealthfront and FutureAdvisor are all the rage now. They invest your money in low-fee index funds for you and reshuffle your portfolio as necessary. That’s a problem for the 10,000 or so investment advisers in the U.S. that are registered with the SEC, however. Younger investors may not go to them, but use a web-based service instead.

Upside, which today announced that it has raised a $1.1 million funding round led by Cultivation Capital, give these advisers a white label solution that’s very similar to what other robo-advisers offer. Prior to this round, the company participated in the St. Louis-based financial tech-focused SixThirty accelerator. Other investors in this round include SixThirty and a number of angel investors, including Suranga Chandratillake (General Partner at Balderton Capital), Elaine Wherry (co-founder at Meebo, acquired by Google), Bruno Bowden (Equity Partner at Data Collective), Noah Tutak (former CEO of Geni and co-founder & CEO of Swim), and Sean Kell (CEO of A Place For Mom, a Warburg Pincus company).

The service was founded by Tom Kimberly, who has background in retail financial services and M&A, and Juney Ham, the former director of online marketing for Airbnb. As they told me last week, they started the service in 2013 with the idea to compete with Betterment and Wealthfront. What they realized, however, was that customer acquisition was very costly. Indeed, Kimberly argued that it would take many of these services between three and four years to break even on a new customer. None of these competitors, however, were going after the existing base of investment advisers who already service a huge number of clients and who are already aware of the threat these services pose to their future business. These advisers have millions of clients and manage billions of dollars in assets already. They also know that younger client my bypass them completely.

“It’s pretty clear that from a generational perspective that younger clients are systematically underserved in the market today,” Kimberly told me. “There is a huge amount of people and assets that are underserved by the status quo.”

Kimberly told me that when they started talking to advisers, it became clear that there was a huge market for a Wealthfront-like service for advisers. Most advisers set certain lower limits for their clients (often a million or half a million dollars), but at the same time, they don’t want to turn away business, either, and somebody who only has a quarter million to invest today may have half a million in a few years.

Just like in most businesses, advisers make eighty percent of the revenue comes from the top twenty percent of customers, so by being able to help their relatively low-value clients manage their assets through Upside’s white-label solution, they get to improve their margins for this group of clients.

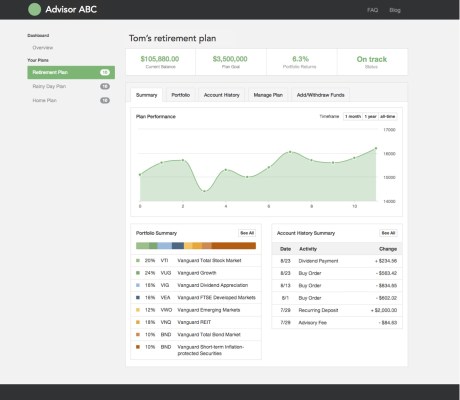

Upside’s default investment strategy is similar to that of other robo-advisory services in that it mostly focuses on low-fee index funds and bond ETFs that are allocated according to a client’s age, expected retirement age and willingness to take financial risks. Advisers can also tweak these strategies, though, and use their own model portfolios. Advisers get a white-labeled portal for their clients and can then be as hands-on or hands-off as they want to be. Upside takes a 0.25% fee for its services and advises its partners to charge less than a 1% fee for their services in total.

Looking ahead, Kimberly and Ham tell me, the company plans to invest its current funding to expand the company’s mostly engineering-focused staff of eight with a larger sales and marketing group that can help it fuel its growth and reach more advisers quickly. The company, of course, will also use these funds to continue to evolve its current product. One thing they co-founders to not expect, however, is to go back into the direct-to-consumer space. “We don’t want to compete with advisers — we want to partner with them,” Kimberly said.

Upside got some early validation for its service recently, too. Shareholders Service Group, a broker/dealer basin in San Diego that provides brokerage services to over 1,200 advisers across the U.S. recently partnered with the company and the company has been talking to some of the major online trading service, too.