These people (the U.S. government) need to be stopped. Every time we get ourselves into an economic mess, there’s usually some milestone idiocy we can point back to as the government action that made the meltdown inevitable.

Take the current housing crisis that has now spread to the financial markets in general. The cause was too-easy credit that fueled a massive increase in housing prices as people bought houses they couldn’t afford with mortgages they weren’t able to pay off.

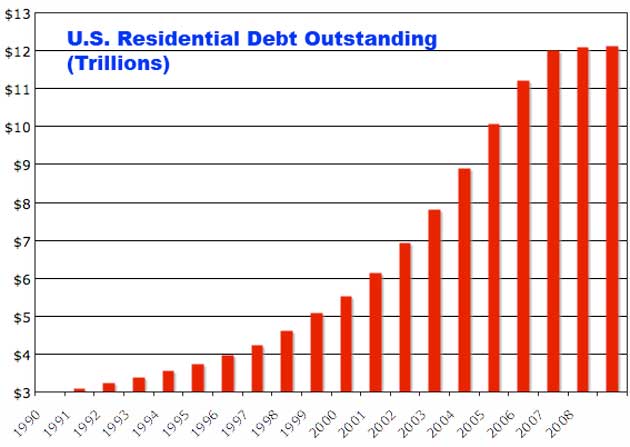

In 1999 there was roughly $5 trillion in total U.S. mortgage debt. That number ballooned to $12 trillion by 2007, and we know what happened from there (data is from the U.S. Office of Federal Housing Enterprise Oversight). To put this into perspective, total U.S. GDP is about $11 trillion annually, and U.S. government debt is around $9 trillion. If the housing market really falls apart (meaning more than conservative estimates of a 20% drop), there’s no way the government can simply cover these losses.

Why did it happen? Let’s go back to 1999, when Fannie Mae, the nation’s biggest underwriter of home mortgages, was under pressure by the Clinton administration to find a way to get more loans to “borrowers whose incomes, credit ratings and savings are not good enough to qualify for conventional loans.” A pilot program was launched, which soon became general policy. Money flowed to people who couldn’t afford to pay it back.

These new policies came on top of previous changes in the 90’s that let consumers get zero-down payment loans.

In a 1999 article that now looks absolutely insane, the New York Times reported on the easing of credit terms. Fannie Mae Chairman Franklin Raines, who’s quoted in the article, was all sunshine and roses as he threw away the financial future of millions of Americans. But at least one person. Peter Wallison, had a good idea of how this would all play out:

In moving, even tentatively, into this new area of lending, Fannie Mae is taking on significantly more risk, which may not pose any difficulties during flush economic times. But the government-subsidized corporation may run into trouble in an economic downturn, prompting a government rescue similar to that of the savings and loan industry in the 1980’s.

”From the perspective of many people, including me, this is another thrift industry growing up around us,” said Peter Wallison a resident fellow at the American Enterprise Institute. ”If they fail, the government will have to step up and bail them out the way it stepped up and bailed out the thrift industry.”

Too bad nobody listened to that guy.